Wednesday, 31 July 2019

Written by Matthew Stuart-Box, COO, Head of Investment Platform

When investors start investing outside of Malaysia it is natural to worry about foreign exchange risk. If you invest in assets denominated in a foreign currency, say US dollars, then your return will depend not only on the return of the asset itself but also on movements in the USD:MYR exchange rate. If the MYR weakens against the USD, your return will be increased but if the MYR strengthens then your return will be decreased.

In other words, the return in MYR terms of a portfolio of USD denominated assets can be seen as having 2 parts:

1) Portfolio Return in MYR = Portfolio Return in USD+Change in USD:MYR rate

There are many benefits of investing in a diversified portfolio of global assets but the question of what to do about the foreign exchange risk is one which concerns many investors. In this blog, we will look at the various ways of dealing with this issue and the approach taken by MYTHEO.

2) Foreign exchange as a source of risk.

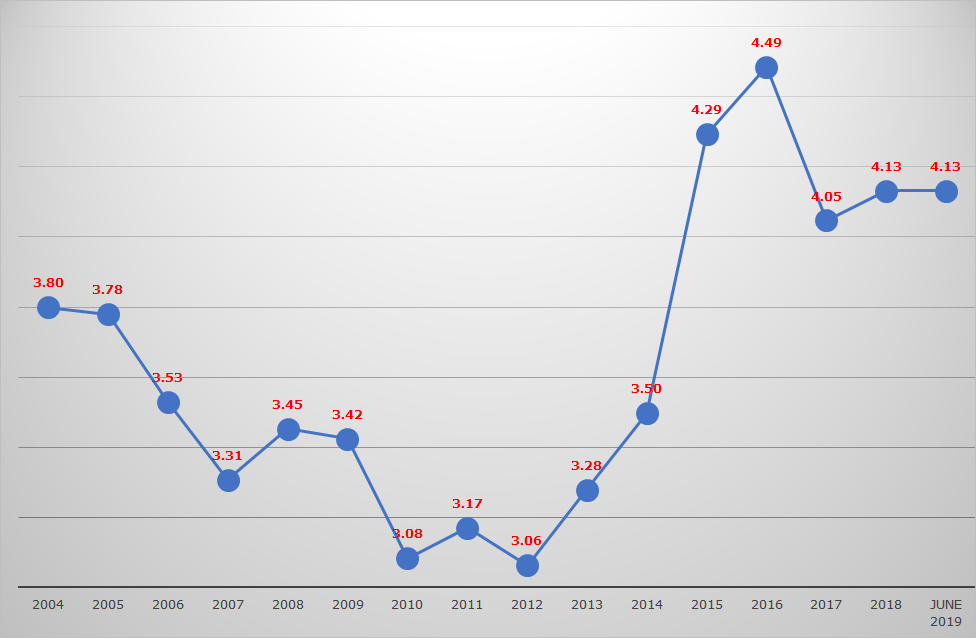

Most people view foreign exchange markets as a source of risk without any compensating return. This appears to be true in the case of USD:MYR. If we look at the long run history since the currency peg was removed in 2005, we see that the rate has moved in a range of roughly MYR3 to MYR4.5 as shown in Chart 1.

Chart 1: USD:MYR Performance from 2004 to June 2019

In Chart 2, as at 31 December 2018, USD:MYR was trading at 4.13, in which USD had risen by 8.8% since the de-peg in 2005. This means that the USD: MYR average annual return was only 0.60% but the risk has been quite high with annual returns of up to 22.8% in the year 2014. In this sense, it is correct to view foreign exchange as a source of risk.

Chart 2: Annual and Cumulative Performance of USD:MYR from 2004 to 2018

Ways to handle foreign exchange risk

What can investors do to handle this risk? There are 3 main options:

1. Hedging

2. Timing

3. Do nothing

Hedging

Hedging involves entering into contracts to sell the foreign currency (e.g. USD) in the future in return for MYR. This offsets the impact of the exchange rate movement since, if the MYR strengthens, the local currency value of your overseas investments will fall but the value of your hedge contract will increase.Hedging can be effective in reducing the volatility of your returns, but it is important to note that hedging involves costs. The cost varies depending on the difference in interest rates between the US and Malaysia, the spread charged by the hedge counterparty and any short-term differences in demand and supply for hedging. These rates change through time but can add up to 1~2% per year.

Timing

This involves taking a view on whether the MYR is likely to strengthen or weaken in the future. If you think the MYR will strengthen then you should hedge the USD exposure. If you think that the MYR will weaken then you should not hedge. In other words, you try to time the moves in the currency and only hedge when it moves against you.This is an attractive concept, but the truth is that it is very hard to do. Currency markets are some of the largest, most liquid and most efficient markets in the world. There are very few people who can consistently predict the movement of currencies.

Do nothing

This involves accepting that currency risk is part of global investing and accepting the short-term volatility of currency exposures in the knowledge that, in the long term, they tend to net out. The obvious advantage of this approach is that it avoids the costs of hedging or the risk of mis-timing currency movements.

The importance of correlations

Many investors think of currency risk on its own. However, it is important to consider the relationship between the returns of the portfolio in USD terms and movements in the USD:MYR exchange rate. In the case of a portfolio of global equities, these returns tend to move in the opposite direction of the USD:MYR exchange rate. In other words, when global equity prices are rising, the MYR tends to appreciate against the USD and when global equity prices are falling, the MYR tends to depreciate. We can see this in the graph below:

Chart 3: Annual Returns of MSCI All Country World Index in USD and USD:MYR

This means that movements in global equity prices and USD:MYR tend to offset each other and hence the annual volatility of portfolio returns in MYR is actually lower than the volatility of the returns in USD and so hedging is likely to give you higher volatility in returns.

Chart 4: Monthly Returns of MSCI All Country World Index in USD and USD:MYR

This means that movements in global equity prices and USD:MYR tend to offset each other and hence the annual volatility of portfolio returns in MYR is actually lower than the volatility of the returns in USD and so hedging is likely to give you higher volatility in returns.

Chart 5: Annual Volatility of MSCI All Country World Index in USD and USD:MYR

What is MYTHEO’s approach to currency risk?

The examples above focus on USD:MYR currency risk. MYTHEO’s portfolios invest in US-listed ETFs and hence are denominated in USD but the underlying assets in the ETFs are global. For example, MYTHEO invests in Global Infrastructure (iShare Global Infrastructure ETF), Global Real Estate (SPDR International Real Estate ETF) and specific country assets in Hong Kong (iShare Hong Kong ETF), Japan (iShare MSCI Japan ETF), United Kingdom (iShare MSCI United Kingdom ETF) and many more. Hence MYTHEO’s portfolios, in addition to diversification over multiple asset classes, have also diversified currency exposures across a range of global currencies including USD, GBP, EUR, JPY etc.

MYTHEO’s approach is to not hedge the currency risk in the portfolios. The reasons for this are as follows:

1. Cost: The costs of hedging currency risk would reduce long-run expected returns for the portfolios. The costs will vary through time, but the compound effect would be to reduce the value of the customer’s portfolios by a material amount.

2. Investment horizon: MYTHEO’s portfolios are designed for relatively long-term investment horizons. In the short run (e.g. a few weeks or months) movements in the exchange rate may impact returns but, in the long run (e.g. over several years), these movements terms to net out and have little impact on total returns.

3. Correlations: Many of the assets in MYTHEO’s portfolios (e.g. global equities) actually have a negative correlation with the USD:MYR exchange rate. This means that the volatility of returns (i.e. risk) of the un-hedged portfolio may actually be lower than that of the hedged portfolio.

Conclusion

In the short run currency risk can have a material impact on MYR returns for a global portfolio so it is natural that investors are concerned about this risk. However, it is important to take a long run view, understand the costs involved in hedging and the impact of the correlation between global assets and the exchange rate and to have a good portfolio of assets diversification. This is part of MYTHEO’s portfolio investment strategy.

On this basis, we believe that not hedging the currency is the approach most likely to give investors the best long-term returns.