Wednesday, 16 March 2022

Written by MYTHEO

Contributed by Dr. Yasuyuki Kato, Director of Money Design Institute, Professor of Kyoto University of Advanced Science, Visiting Professor of Kyoto University and Specially Appointed Professor of Tokyo Metropolitan University who also sit on the board of Japan’s Government Pension Investment Fund.

Russia's invasion of Ukraine has shaken financial markets. For the time being, it seems better to be prepared for asset price volatility to increase. Some investors may feel scared and want to liquidate all of their investment portfolio. However, past history has repeatedly taught that this would miss a major opportunity in terms of long-term investment.

So, what do long-term investors think? This time, let's think about how investors should deal with this situation.

In considering how to deal with this situation, it is first necessary to have a good understanding of the characteristics of asset prices, in particular a phenomenon known as "mean reversion". Asset prices fluctuate, but tend to return to their averages over time.

In other words, if a price goes up, it subsequently goes down, and if a price goes down, it subsequently goes up. Of course, asset prices such as stock prices tend to rise in the long run, but in the process they will rise and fall. If an asset has real value, the price tends to meander around it.

In particular, in the event of a major shock like this one, the market tends to over-react and the fluctuations tend to be larger than necessary. However, given the phenomenon of mean reversion, the investor’s response to the shock is clear. In other words, you can sell the assets that have gone up and buy the assets that have gone down. This buying and selling is especially easy for diversified portfolios.

In an internationally diversified portfolio, such as MYTHEO, it is common for parts of the portfolio to react negatively to the shock and parts to react positively at the same time. In fact, even in this shock, for example, the price of stocks has fallen while the price of gold and oil has risen. If the prices of these assets return to the average, you can sell the ones that went up and use that cash to buy the ones that went down.

In other words, if you hold a range of assets with a certain asset allocation ratio, you can transfer the funds from the assets whose prices have risen to the assets whose prices have fallen and return to the original asset allocation ratio. If you do this for all your assets at the same time, no additional funding is required. This is called rebalancing and is one of the basics of long-term investors with diversified portfolios. By the way, it is also one of the important functions of MYTHEO.

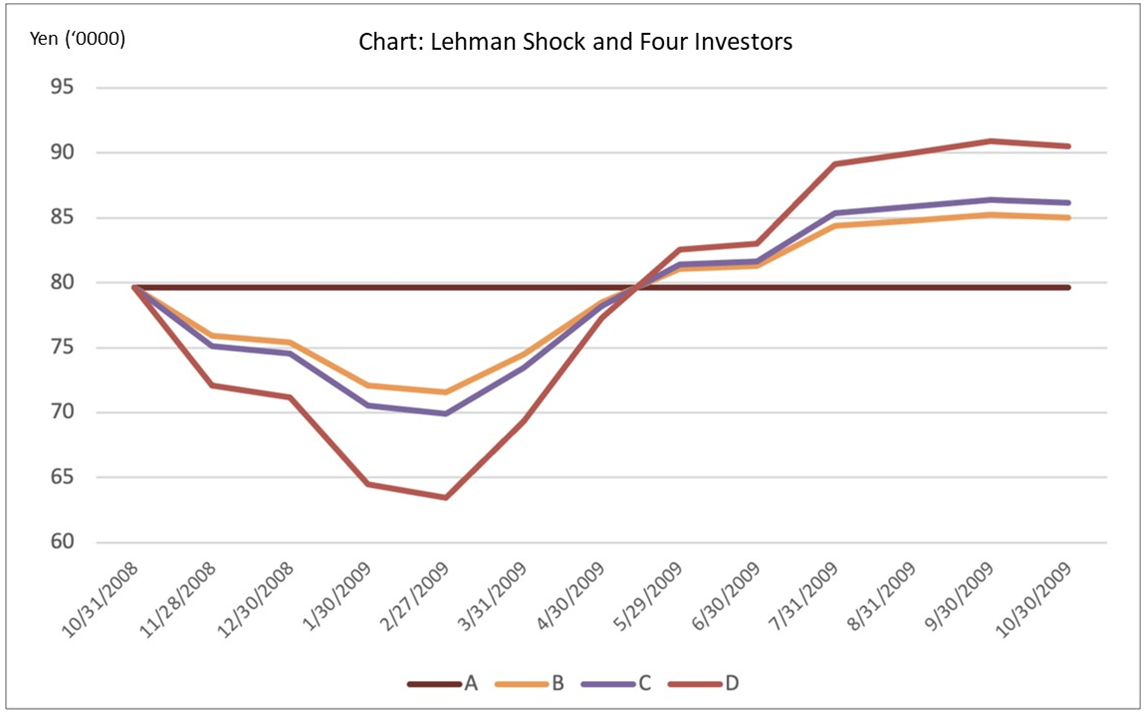

Let's simulate the effect of rebalancing by taking the Lehman shock, in which stock prices fell by up to 50%, as an example.

Imagine four virtual investors, Mr. A, Mr. B, Mr. C, and Mr. D who all held cash of 400,000 yen and global stocks of 600,000 yen (total of 1 million yen) just before the Lehman shock occurred at the end of August 2008. Assume that their global stocks are the same as the MSCI-ACWI index. The allocation ratio is 40% in cash and 60% in global stocks. And when the Lehman shock occurred in September, the world stock price (MSCI-ACWI index) fell by 36% at the end of October, so the assets of the four people all fell to 400,000 yen in cash and 400,000 yen in stocks, totalling 800,000 yen. From there, the four take different actions:

Mr. A: Sell the global stocks held and hold all assets in cash (cash will be 800,000 yen)

Mr. B: Do nothing and leave it as it is (cash 400,000 yen, stock 400,000 yen)

Mr. C: Buy more stock with a part of cash (80,000 yen) (cash 320,000 yen, stock 480,000 yen)

Mr. D: Buy more shares with all the cash held (400,000 yen) so that stocks will total 800,000 yen

Now let's examine the performance of these four people for the next year (end of October 2008 to the end of October 2009). Transaction costs are not included. The chart shows the changes in the assets of the four people.

Stock prices continued to fall after October 2008, but subsequently stated to turn up. The amount of assets as of the end of October 2009 compared to the amount of assets as of the end of October 2008 was unchanged for Mr. A who only held cash, it increased by 6.8% for Mr. B, increased by 8.2% for Mr. C, and for Mr. D it increased by 13.6%.

In other words, the more stocks you buy, the more your total assets recover. On the contrary, Mr. A, who thought it was safe and cashed everything, ends with the least amount of assets. This was an example of the Lehman shock, but it can be said that other shocks that have occurred so far have the same tendency, even if there is a difference in timing. So mean reversion happened each time.

By the way, Mr. C's behaviour (buying more stock with cash of 80,000 yen) is actually the same as rebalancing. As already mentioned, rebalancing is the restoration of the asset allocation ratio that has deviated due to fluctuations in asset prices. The original asset allocation of the four people was 400,000 yen in cash and 600,000 yen in stocks. However, due to the plunge, the allocation changed to 400,000 yen in cash and 400,000 yen in stocks, and when converted to an allocation ratio, it changed to 50% in cash and 50% in stocks. Therefore, Mr. C transferred a part of the cash (80,000 yen) into stocks, and set the cash to 320,000 yen and the stock to 480,000 yen (i.e. 40% for cash and 60% for the stock) to return to the original asset allocation ratio. One option is to put all the cash into the stock and take the plunge like Mr. D, but there is also the risk that the plunge will continue. In fact, Mr. D's assets continued to fall sharply. Mr. C's investment behavior of rebalancing is an excellent way to make good use of mean reversion while keeping the risk level at a level that suits him. By the way, this concept of rebalancing is almost always included in the investment policy documents of major institutional investors such as pension funds. Successful pension funds have been quietly rebalancing in the face of major shocks.

Timing of rebalancing

By the way, the difficult part of this rebalancing is the timing of rebalancing. We want to sell the assets we sell at high prices, and we want to buy the assets we buy at low prices. However, not many people can buy and sell at such an ideal time. In some cases, you may end up rebalancing with terrible timing and sell just before prices go up or buy just before prices go down.

The important thing is to continue rebalancing regularly over the long term. If you continue to rebalance for a long period of time, sometimes the timing will be bad and sometimes the timing will be good. These timings are random and you will end up with rebalances at an average timing and this average is sufficient for long-term investments.

This rebalancing is also done regularly at MYTHEO. It's a modest task, but it's the most important feature for improving the performance of long-term investments. In other words, the best way to deal with a shock is to rebalance as usual without over-reacting.

* 1) MSCI-ACWI: The world stock index published by MSCI includes 23 developed countries and 24 emerging markets.

* The opinions and opinions expressed in this article are those of the author and are not the official opinions of MYTHEO and MONEY DESIGN Co., Ltd.

* Article has been translated from Japanese. Source:https://note.theo.blue/n/nb25491fa89c0

This material is subjected to MYTHEO's Notice and Disclaimer.