Friday, 9 April 2021

Written by Amirudin Hamid, Portfolio Manager of GAX MD

March 2021 wrapped up with negative news all throughout the month. The third wave of the COVID-19 outbreak hit Europe, forcing Germany and France to tighten measures to contain the virus. The problem in Europe was aggravated further by the delay in the vaccination program due to supply issues and safety concerns over the vaccine developed by AstraZeneca.

Treasury yields continued to climb higher. The benchmark 10-year treasury notes leapt to yield 1.744% at the end of March. Federal Reserve Chairman, Jerome Powell tried to play down the threat of inflation during the meeting with the US Congress. At the same, Mr Powell reported that the Federal Reserve expects the inflation rate to reach 2.4% in 2021. Mr Powell’s statement was not well received by the investment community. The investment community was worried that the Federal Reserve may have to play catch-up again by hiking rates aggressively, similar to the situation in 2018. Despite that, Mr Powell’s reiteration of the pledge to keep the interest rate low resulted in bond yields spiking and the stock market trading downwards post the meeting.

The relationship between the US and China was in limbo once again. On 22 March 2021, the US, with the support from its key allies including UK, the European Union and Canada, imposed a sanction on Chinese officials over the Xinjiang region issues.

Stock markets were hit by another blow-up, this time, involving a hedge fund called Archegos Capital Management that resulted in more than US$20 billion in force liquidation of stocks in the US. The event inflicted billions of US Dollars in losses to several well-known global banks. Additionally, several shares that were linked to Archegos were severely affected. Some examples were GSX Techedu, Discovery Communication, ViacomCBS and iQiyi, which plummeted by more than 40% in just one week.

However, there was some good news that came out of US President Joe Biden's office. Firstly, the long-negotiated US$1.9 trillion fiscal package was finally passed by the House of Representatives and signed off by Mr Biden on 11 March 2021. On 31 March 2021, Mr Biden announced a plan to develop US$2.3 trillion worth of infrastructure projects over the next eight years. The announcement created more excitement and optimism in the market.

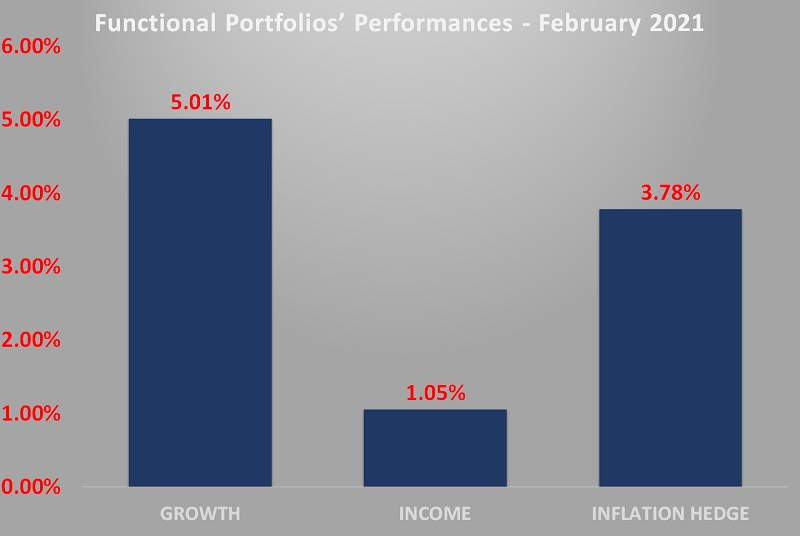

MYTHEO’s portfolios had a good month in March 2021. The Growth, Income and Inflation Hedge portfolios jumped by 5.01%, 1.05% and 3.78% respectively.

Chart 1: Functional Portfolios' Performances for month of March 2021

Source: GAX MD Sdn Bhd, April 2021

Note: Past performance is not an indication of future performance

The GROWTH portfolio rose by 5.01% in MYR

The US market made a comeback in March 2021. However, the components that drove the market’s performance were not the growth and work-from-home stocks.

Instead, the new winners were laggard stocks that were trading at cheap valuations, which are known as "value" stocks. These included stocks from the banking, telecommunication, utilities and energy sectors that the market had ignored in the chase for growth stocks.

As a result, Value stocks ETF (VTV) spiked up by 9.16% in March 2021. Meanwhile, US companies with high environmental, social and governance (ESG) factor scores ETF (SUSA) was up by 7.35%. Technology stocks only accounted for around 30% of total holdings in SUSA. The remaining 70% of exposure were investments from sectors such as, communication, consumer, industrial and real estate that were trading cheaply.

Increasing appetite towards "value" had also favoured the Singapore market (EWS), which ticked up higher by 8.61%. EWS holds banking and telecommunication stocks that did not move along with the rally of technology stocks in the last upcycle.

Also, from a valuation perspective, the Singapore market was still trading at a low Price-to-Earnings (P/E) ratio of 14.6x, which is cheap compared to VTV that was trading at P/E ratio of 30x.

The only loser in the Growth portfolio was China stocks (FXI) which was down by 2.68%. Investors in China faced more jitters after the US and its allies sanctioned two Chinese officials over the Xinjiang region issues, a move that could sour the relationship between both parties.

The INCOME portfolio rose by 1.05% in MYR

Overall, a stronger US Dollar provided support to the performance of the Income portfolio in March 2021. The US Treasuries across all expiry dates continued to trend downwards as yields kept on rising.

The US Treasury, with a long time to maturity was hit the hardest due to high sensitivity to yields. At the month-end, the US Treasury with more than 20 years to maturity (TLT) dropped by 3.02%.

Some parts of the portfolio were negatively affected by the stronger US Dollar, particularly the non-US Dollar bonds. The Emerging Market bonds traded in its home currency (EMLC) was down by 0.64%, while the International Treasury Bonds (BWX) dropped by 0.21%.

On the contrary, higher risks bonds continued to perform better due to a more robust appetite for risks. High Yield Corporate Bonds (HYG) and Short-term High Yield Corporate Bonds (SJNK) were up by 3.75% and 3.59%, respectively.

The INFLATION HEDGE portfolio increased by 3.78% in MYR

Investors placed more bets on potential winners from inflation, which pushed the real estate and infrastructure-related stocks higher.

Real Estate Mortgage (REM), US Real Estate (IYR) and Global Infrastructure (IGF) all had solid monthly gains of 8.55%, 8.25% and 7.30%, respectively.

Profit-taking on high-flying ETFs continued to affect some ETFs inside the Inflation Hedge portfolio. Silver (SLV) dropped by 8.5%, and Clean Energy (ICLN) went further down by 6.43% in March 2021, but over one year, both ETFs still carried net gains of 67.8% and 160%, respectively.

It must be noted that, the actual portfolio returns to the investors is the combined weighted return from the allocation to each functional portfolio. For example, if an investor has an investment allocation of 40% in Growth, 40% in Income and 20% in Inflation Hedge, the actual portfolio return is (40% x 5.01%) + (40% x 1.05%) + (20% x 3.78%) = 3.28%

Note: Past performance is not an indication of future performance

Our thoughts

After a below-par performance in the past few months, the US stock market picked up from where it had left off last year. However, technology and work-from-home stocks were not at the heart of the market upcycle in March 2021. Instead, stocks that had been trailing behind during the last rally and trading at cheaper valuations were the ones that moved the market up.

MYTHEO’s Growth portfolio invests in equity ETFs, and about 50% of total exposure is in the US. While MYTHEO has been investing in high growth technology stocks, our portfolio has never ignored the "Value" and "ESG" (Environmental, Social and Governance) stocks.

That worked very well, as Vanguard Value (VTV) jumped by 9.16% and the Growth portfolio rose by 5.05% in March 2021.

Separately, many investors are starting to worry about the US treasury yields that have been rising over the past six months. In March 2021, the yield hit 1.70% for the first time since February 2020.

This trend has negatively impacted some parts of MYTHEO holdings, particularly the Treasury ETFs. Over the past 6 months (Oct 2020 – March 2021) this high yield trend has brought down the Income portfolio to a marginal loss of 1.81%. However, the Growth and Inflation Hedge portfolio rose by 20.49% and 10.36% over the same period.

MYTHEO’s Functional Portfolios’ Performance over 1-month, 3-month and 6-month Period Ending 31 March 2021

Source: GAX MD Sdn Bhd, April 2021

Note: Past performance is not an indication of future performance

The scenarios above show how diversification in MYTHEO can benefit investors over the long run.

Firstly, it helps investors to avoid being overly exposed to any single theme, and when the market sentiment rotates to different theme, investors will not miss out. Despite the strong performance of the technology sector in the US last year, MYTHEO still invested in "Value" and "ESG" stocks that eventually performed better this year.

Secondly, diversification helps to cushion the impact of a negative market environment. The rising treasury yields environment might have some negative impact to the Income portfolio, but investors who chose the “Omakase” portfolio would have been investing in all functional portfolios. The strong performances of the Growth and Inflation Hedge portfolios more than offset marginal losses in the Income portfolio.

This material is subjected to MYTHEO's Notice and Disclaimer.