26 February 2026

Written by Amirudin Hamid, Chief Investment Officer of GAX MD

Key Takeaways

- From April 2024 to January 2026, the US Dollar weakened by 17.4% against the Ringgit. Despite this significant currency headwind, MYTHEO portfolios remained positive, as asset gains across global markets more than offset translation effects.

- The sell-off in US software stocks, strength in the Ringgit, and correction in precious metals were symptoms of a global rotation. Capital moved toward AI hardware, semiconductors, and commodity-linked economies, particularly in South Korea, Taiwan, and Brazil.

- Exposure to markets where both assets and local currencies performed well amplified returns in USD and MYR terms. Over time, disciplined global diversification allows asset growth to dominate short-term currency volatility.

If you relied solely on financial headlines in January and early February 2026, it would have felt as though markets were coming apart.

Global software giants suffered sharp double-digit sell-offs.

The Ringgit strengthened aggressively against the US Dollar, raising fears of currency losses on overseas investments.

Then, as February began, precious metals experienced what many described as a “flash crash”.

Taken together, these developments painted a troubling picture.

Yet for MYTHEO investors, the lived experience was very different. January turned out to be a record-breaking month. Even more striking, this resilience occurred against a backdrop of sustained US Dollar weakness. From April 2024 to January 2026, the Dollar declined by 17.4% against the Ringgit.

This disconnect between market anxiety and portfolio outcomes highlights an important reality: global capital was not retreating. It was rotating.

A Financial World Moving BeyondUS-Centric Leadership

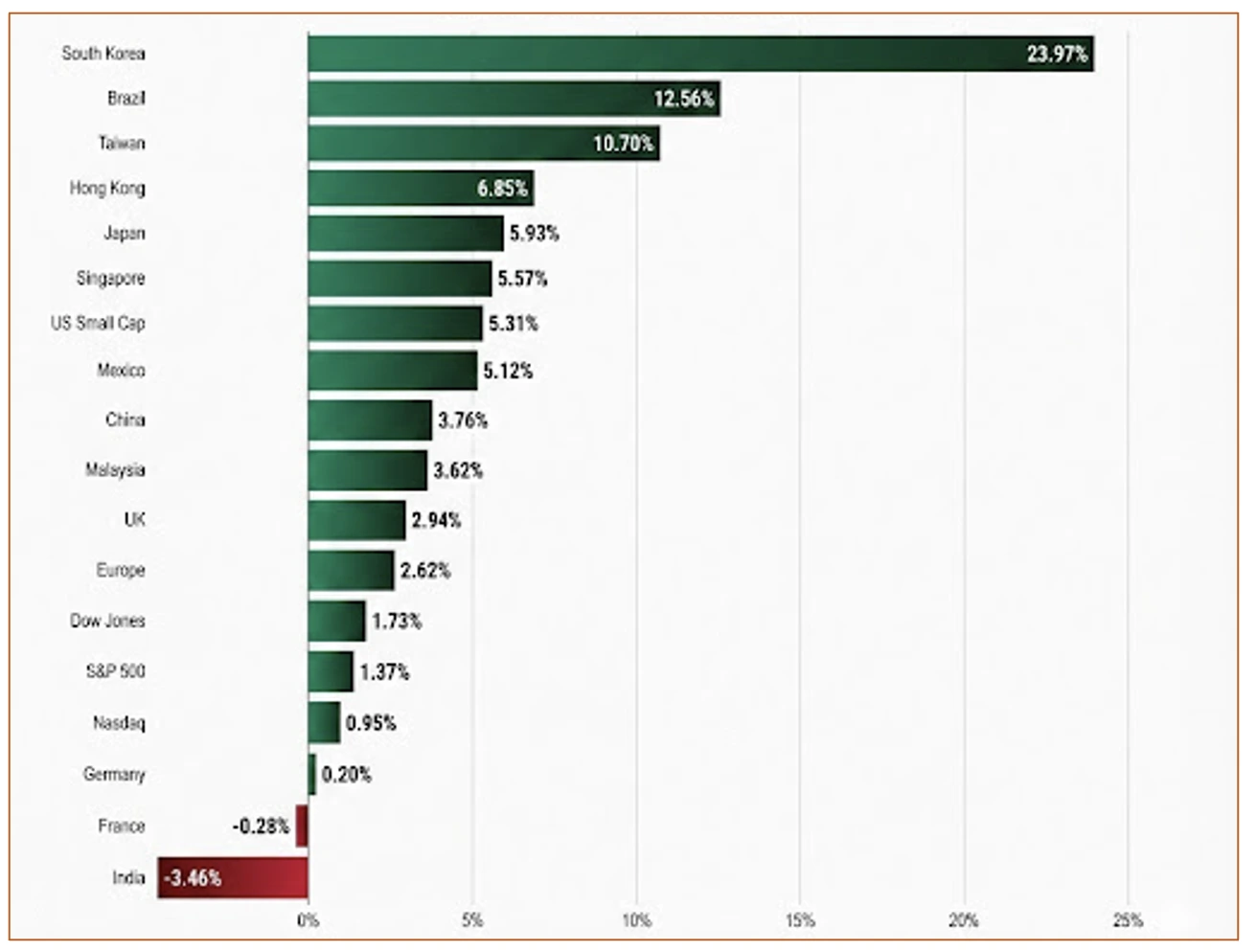

US equity markets started 2026 on a positive note, but their performance lagged behind the rest of the world. TheDow Jones Industrial Average rose 1.73 %, extending its winning streak to nine consecutive months. The S&P 500 gained 1.37 %, while the Nasdaq Composite added 0.95%.

The US market returns were decent, but modest when compared to the explosive rallies seen elsewhere. South Korea,Brazil, and Taiwan posted double-digit gains. Among the markets we monitor, the US outperformed only Germany, France, and India.

Chart 1: Selective Market Performance in January 2026

Source: Gax MD Sdn Bhd

This was not a market sell-off. It was a rotation.

Investor conviction shifted toward the global backbone of artificial intelligence. Capital flowed into hardware manufacturers, semiconductor leaders, and industrial enablers outside the US.Companies such as Samsung Electronics, SK Hynix, TSMC, and ASML became the primary beneficiaries.

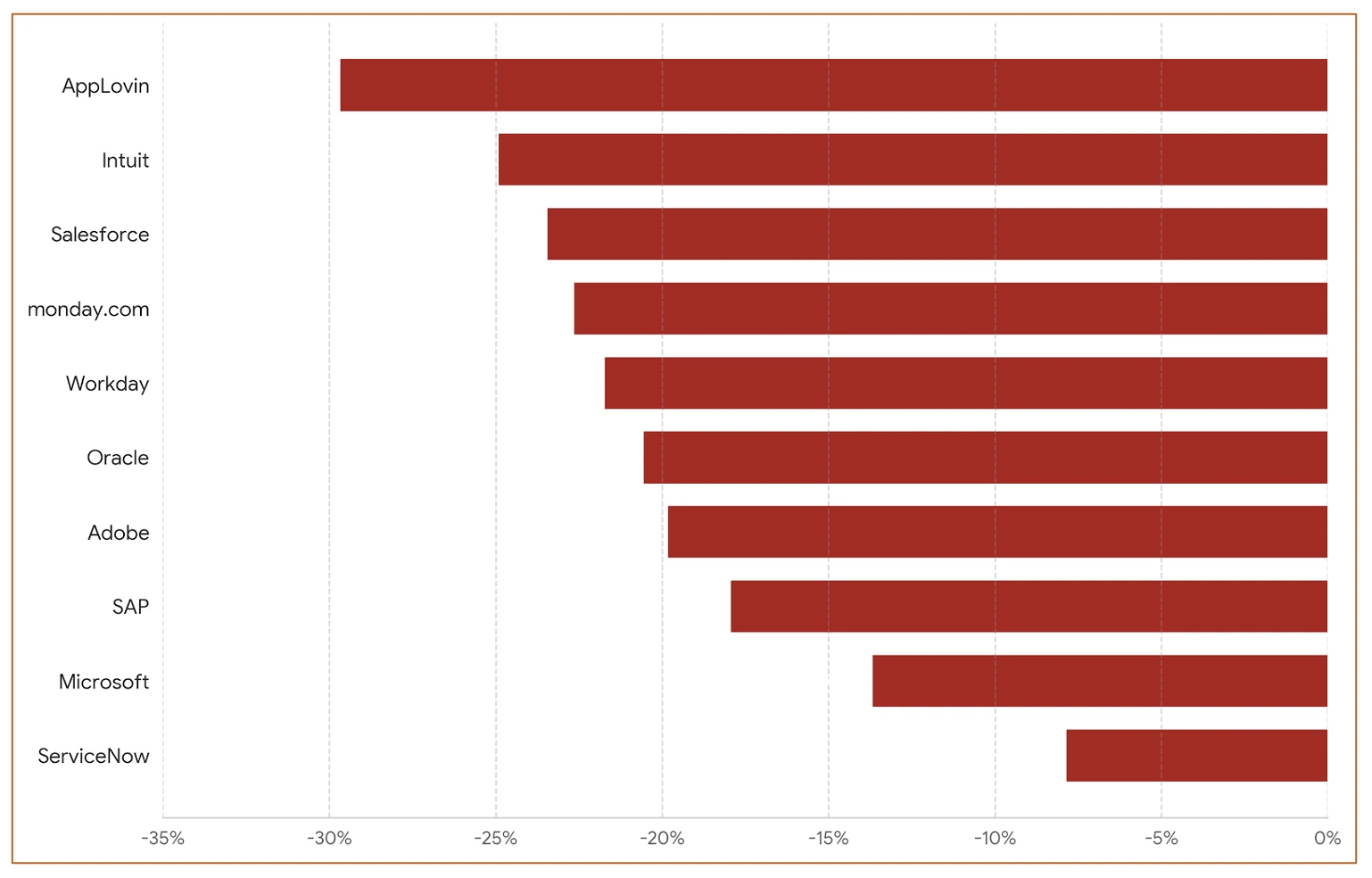

The Tech Wreck: Why the Software Sell-Down Did Not Break Portfolios

January was punishing for the giants of the software world. Heavyweights like Microsoft, Adobe, and Salesforce fell between 10% and 30%.

The fear was existential. Investors suddenly questioned whether artificial intelligence was merely a productivity tool or a direct replacement. If AI agents could write code, manage sales pipelines, and design content, what happens to traditional SaaS subscription models?

MYTHEO portfolios held firm because we do not rely on a single future outcome.

While markets punished companies at risk of being disrupted, they aggressively rewarded the companies doing the disrupting. Chip designers, semiconductor manufacturers, and AI infrastructure providers saw powerful gains. Our Global Growth portfolio is built to capture the entire ecosystem, not just one layer of it.

Losses in vulnerable software names were offset by solid gains in the hardware and infrastructure companies powering theAI transition. This balance is how MYTHEO portfolios are designed to survive regime shifts, rather than betting blindly on yesterday’s winners.

Chart 2: Performance of Major Software Companies in January 2026

Source: Gax MD Sdn Bhd

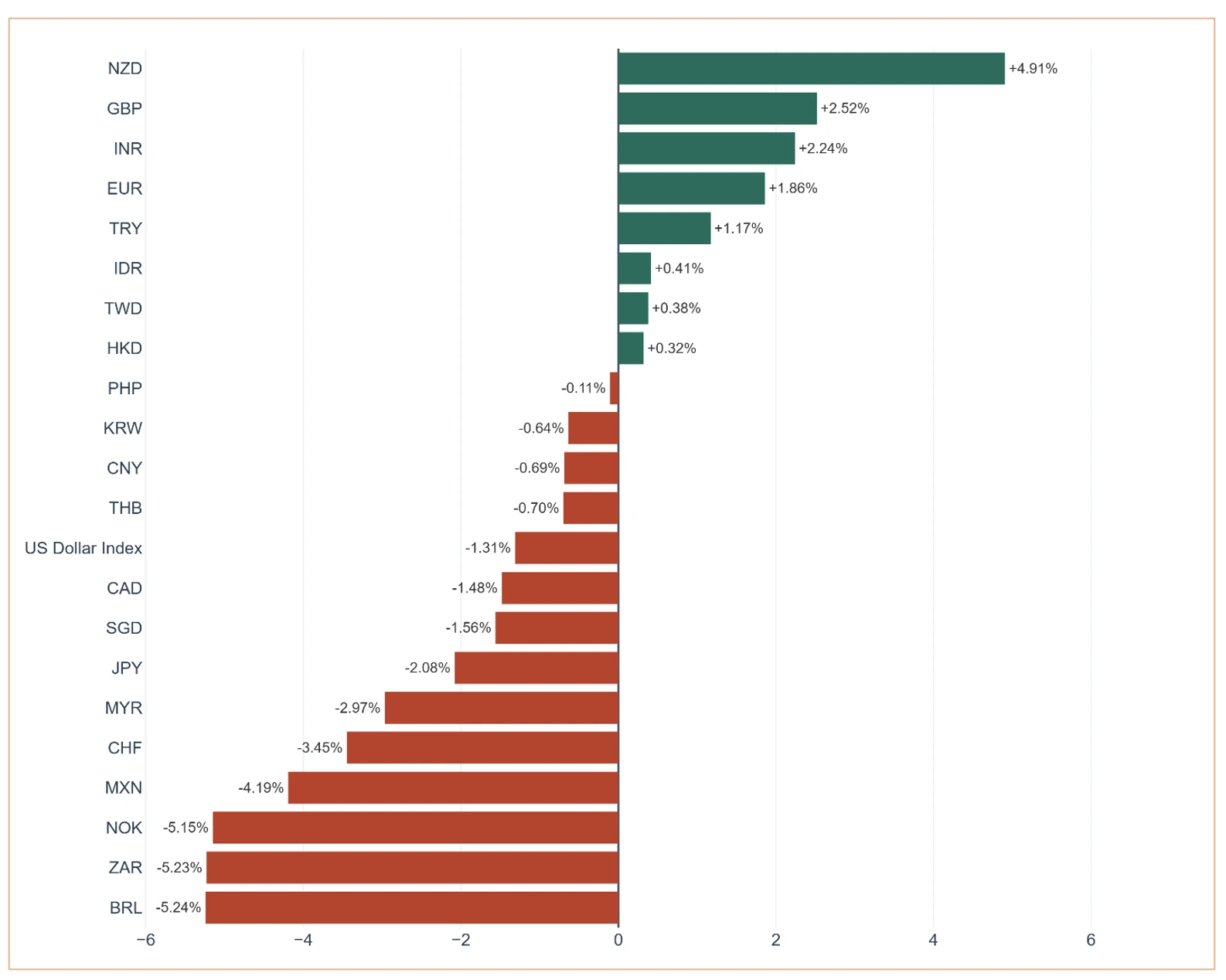

The Ringgit Strength and Overseas Exposure

For the first time since June 2018, the US Dollar fell below the psychological 4.00 level against the Ringgit. In January alone, the Dollar weakened by nearly 3%.

For many Malaysian investors, the reaction was immediate:

“If my investments are in USD, doesn’t a weaker Dollar mean my portfolio must be losing value in Ringgit terms?”

In fact, the opposite occurred. Global equities, infrastructure, and real assets rose strongly enough to overwhelm currency effects, delivering positive returns even after conversion back to Ringgit. Currency is only one variable. When asset performance is robust, exchange rates become a secondary consideration.

Importantly, several emerging-market currencies strengthened even more than the Ringgit. TheSouth African Rand, Brazilian Real, and Mexican Peso all posted strong gains.Exposure to markets with strengthening currencies amplified local assetreturns, resulting in higher portfolio values in both USD and MYR terms.

In addition, many global companies held within the portfolios generate substantial revenues in these regions. Currency appreciation therefore enhanced earnings translated back into USD and Ringgit, further supporting portfolio performance.

Chart 3: US Dollar Performance Against Global Currencies

Source: GAX MD Sdn Bhd,

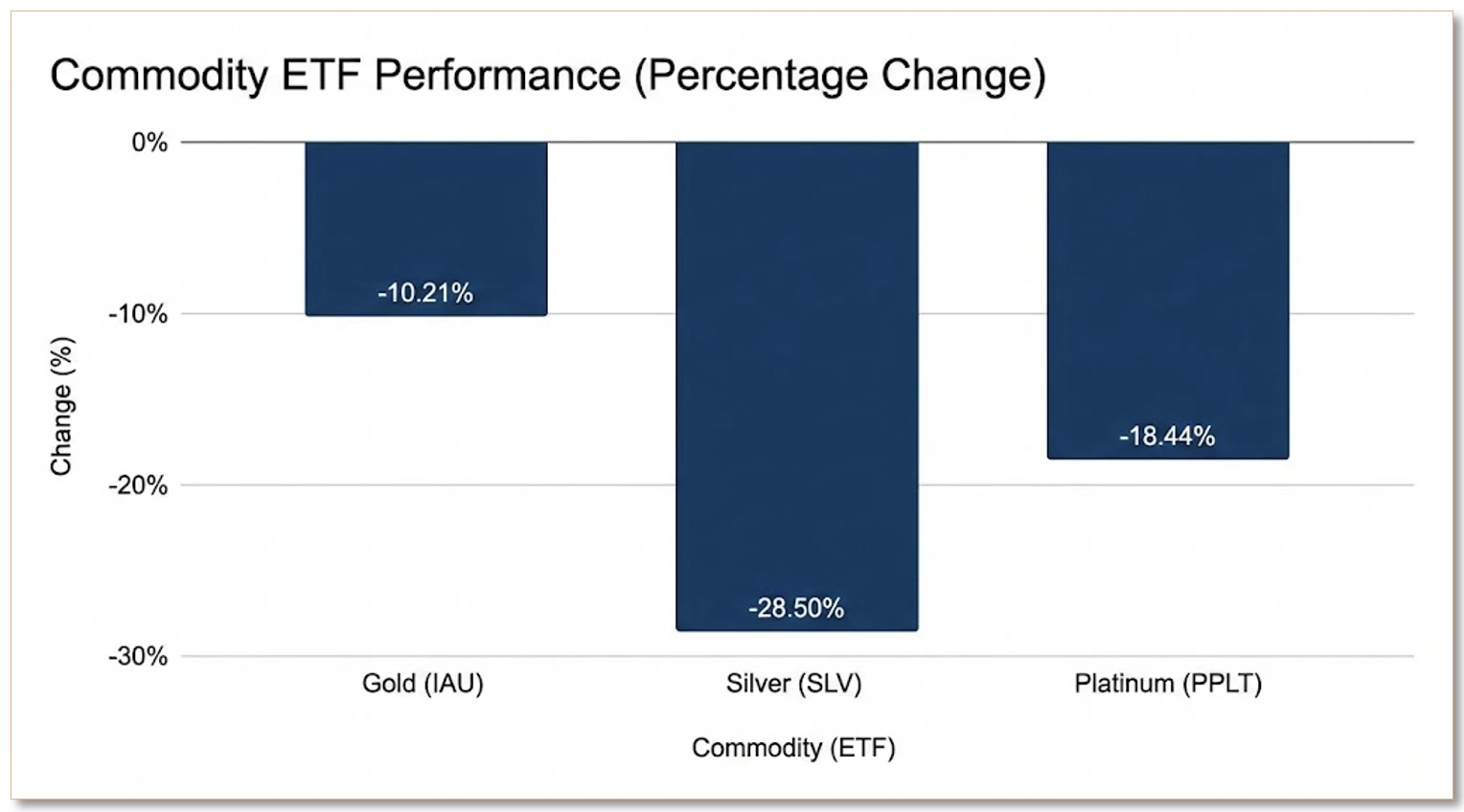

The Precious Metals Sell-off: Volatility or Shift?

After a volatile January, the market buckled right at the beginning of February with a sharp correction in the precious metals sector a move that captured headlines globally. Gold (IAU) fell 10.21%, silver (SLV) dropped 28.50%, and platinum (PPLT) declined 18.44%.

Chart 4: Precious Metal PricePerformance on 1 February 2026

Source: GAX MD Sdn Bhd

This “flash crash” was driven by a convergence of factors: a more hawkish Federal Reserve outlook, a sudden increase in CME margin requirements that forced leveraged liquidations, and trading restrictions in China that curtailed speculative momentum.

The spark for the collapse was the surprise announcement on January 30, 2026, that Kevin Warsh would likely become the next head of the US Federal Reserve. To investors, Warsh is known for being "hawkish", meaning he prefers higher interest rates and a stronger dollar. This changed the game instantly. Because gold and silver don't pay interest or dividends, they became much less attractive compared to US government bonds, which were suddenly promising higher returns. As big institutions rushed to move their money into those higher-paying bonds, they sold off their precious metals all at once, creating a wave of selling that the market simply couldn't absorb.

This initial pressure was made worse by a technical rule change at the CME Group (the world’s largest financial exchange). Think of a "margin" as a security deposit you pay to trade. On January 30, the exchange suddenly raised the cost of these deposits. When the market opened on February 1, many traders were told they had to come up with massive amounts of extra cash immediately. Those who couldn’t find the cash were forced to sell their gold and silver at any price just to stay afloat. This created a "domino effect": as they sold, prices dropped further, which triggered even more forced selling.

To make matters worse, the usual buyers who step in when prices drop were nowhere to be found. Normally, when Western markets sell, buyers in China and across Asia step in to "buy the dip." However, just days earlier, the Shanghai Futures Exchange had restricted trading to cool down speculation. Combined with new export rules, these restrictions effectively "locked the doors" to the market. When the wave of selling hit on February 1, there was no one on the other side to buy, causing prices to fall much further and faster than they normally would.

We view this episode as situational rather than structural. Precious metals are inherently volatile, and moves of this magnitude remain within expected ranges for real-asset strategies. Our algorithms are designed to navigate such episodes, ensuring that the Inflation Hedge portfolio continues to serve its long-term role rather than reacting to short-term dislocations.

Conclusion

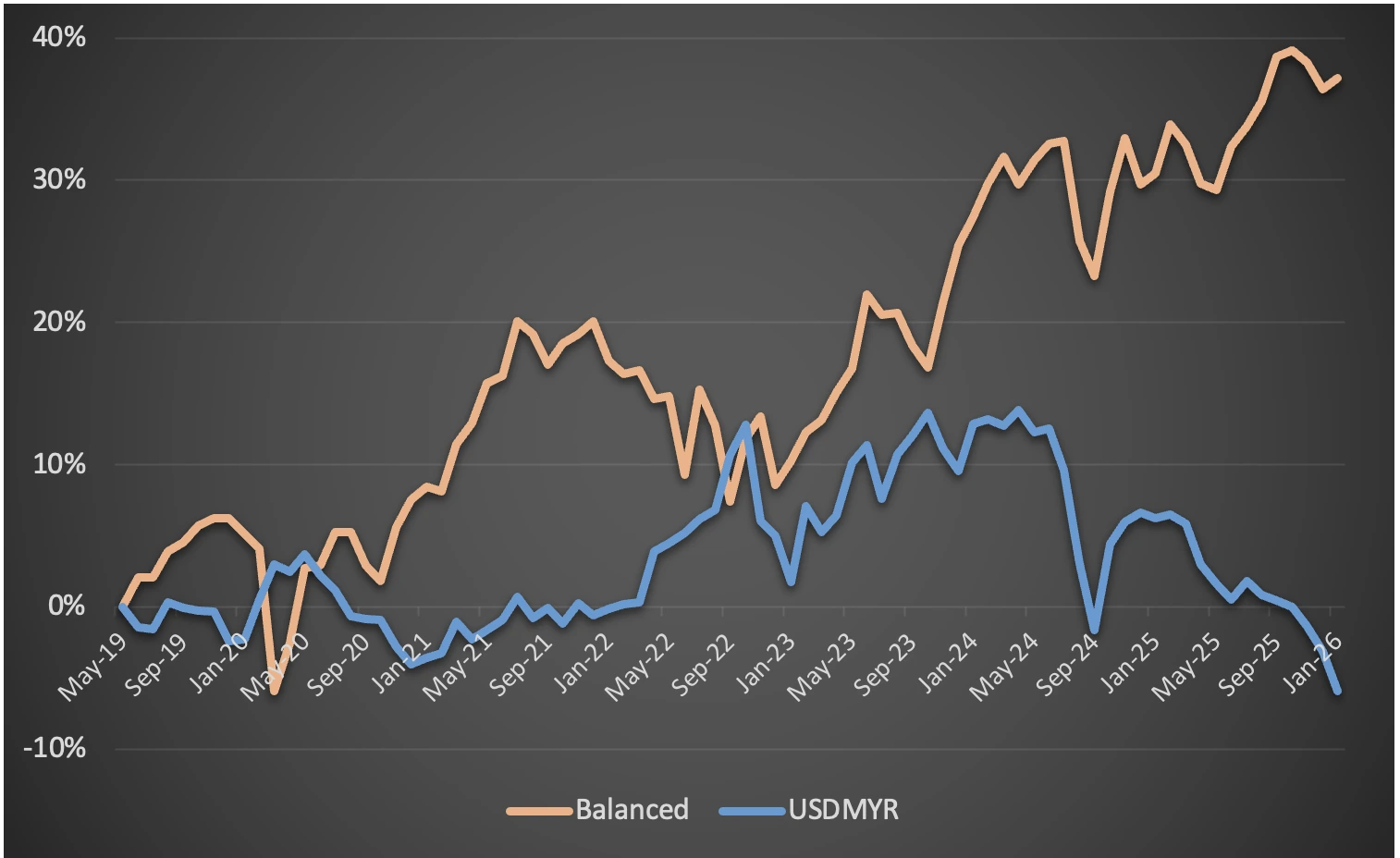

Evaluating the Malaysian Ringgit requires a clear view of how global markets have evolved in recent years. By the end of January 2026, the Ringgit traded at about 3.9250 against the US Dollar. This reflects a meaningful appreciation from the 4.184 level recorded when the Omakase portfolios were launched in May 2019.

This improvement took place during a period when the US Dollar weakened steadily from the inception of the Omakase portfolios through early 2026. Even with this shift, our balanced portfolios, built from Growth, Income and Inflation Hedge strategies, continued to deliver positive performance, as shown in Chart 5.

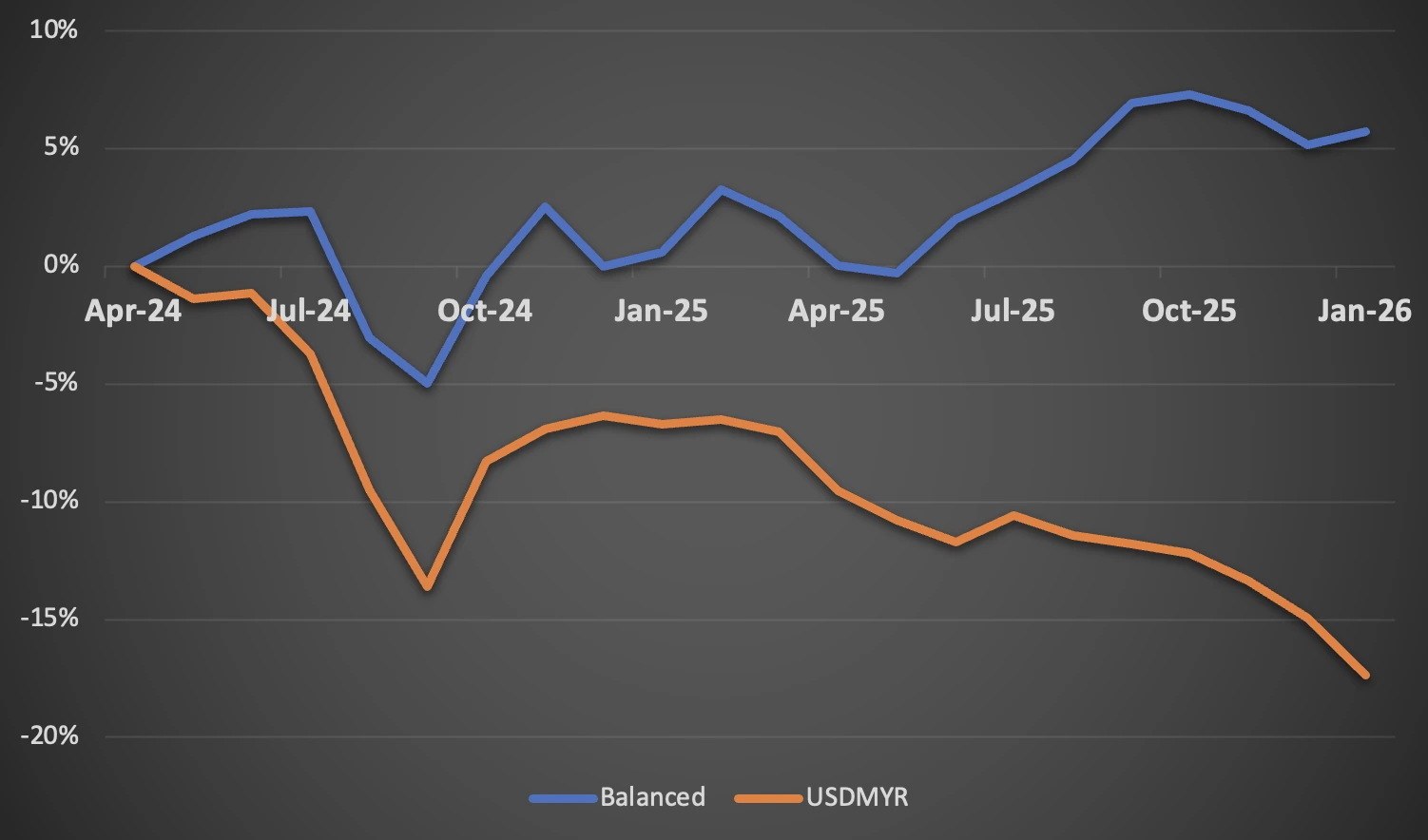

The current USDollar down cycle began in April 2024. From the end of April 2024 to the end of January 2026, it fell by 17.4%, as illustrated in Chart 6. Despite this sizeable translation loss, the balanced portfolio still produced gains when measured in Ringgit.

Chart 5: MYTHEO Balanced Portfolio and USD/MYR Since Inception in May 2019

Source: GAX MD Sdn Bhd

Note: Past performance is not an indication of future performanceBalanced allocation consists of 30% Growth, 47%Income and 23% Inflation Hedge

Chart 6: MYTHEO Balanced Portfolio and USD/MYR Since April 2024

Source: GAX MD Sdn Bhd

Note: Past performance is not an indication of future performanceBalanced allocation consists of 30% Growth, 47%Income and 23% Inflation Hedge

One of the key drivers behind the Dollar’s weakness was the resurgence of commodities. The Dollar often behaves as a defensive asset, while commodities tend to strengthen when global growth improves. When commodity prices rise, capital typically moves away from the Dollar and into growth‑linked markets.

This trend was reflected in the strong performance of currencies such as the Brazilian Real, South African Rand and Norwegian Krone.

For MYTHEO investors, this environment supported portfolios with commodity exposure. The Inflation Hedge and Essential portfolios recorded their strongest monthly performance since inception.

Separately, although MYTHEO invests through ETFs, the underlying exposure is far from passive. Our holdings span markets such as South Korea, Taiwan, China, South Africa and Brazil. These include global leaders like Samsung Electronics, SK Hynix and TSMC, along with major companies tied to emerging market internet growth and commodity‑linked economies.

January 2026 marked an important transition. The long-standing dominance of US technology is giving way to a more globally distributed growth cycle. Policy uncertainty continues to weigh on US markets, while the rest of the world is increasingly finding its footing.

MYTHEO’s Omakase approach ensures that capital is not confined to one country or one theme but positioned to participate in the most compelling growth opportunities wherever they emerge.

"Discover how MYTHEO can enhance your portfolio diversification today and embark on your financial journey with confidence.

Take the first step towards your financial goals now.

Download the MYTHEO app in the iOS App Store or Google Play store.

Or visit mytheo.my to learn more."

This material is subject to MYTHEO’s Notice and Disclaimer.