Key Takeaways

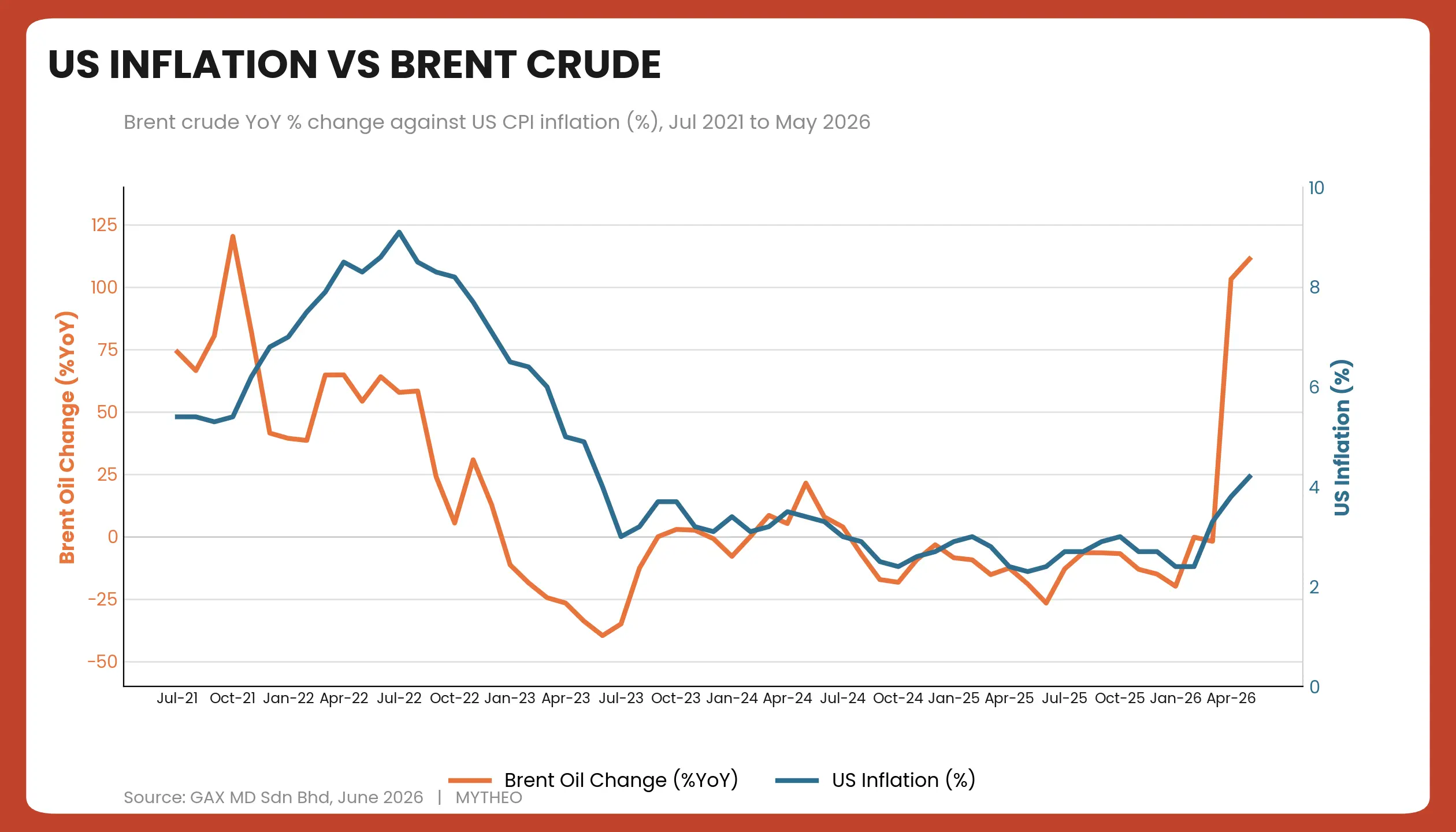

- The progress toward a US Iran ceasefire drove a 29% decline in Brent crude oil, confirming that recent inflationary spikes are primarily linked to energy costs rather than broad based economic overheating.

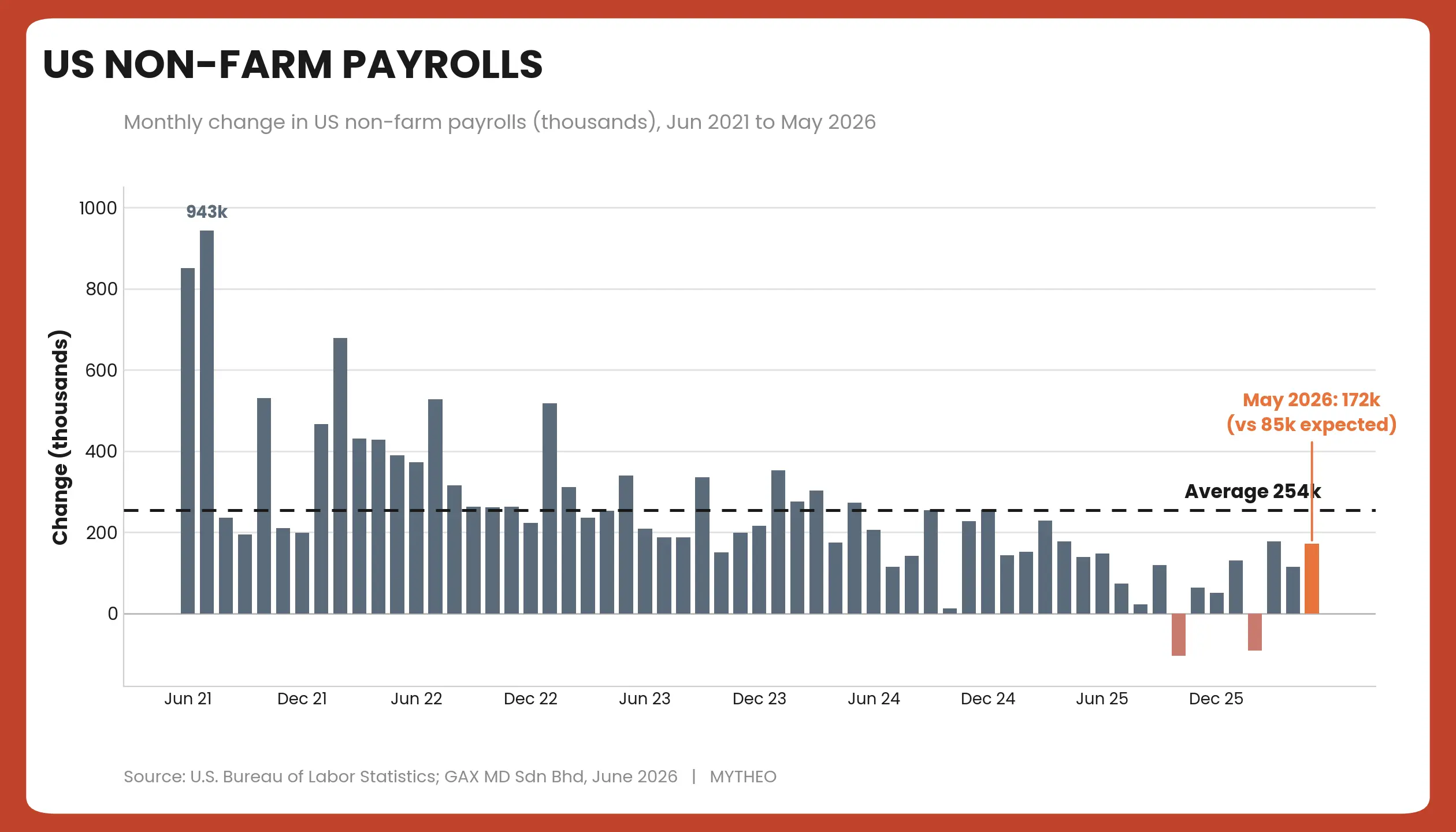

- Despite rising inflation and volatility in non-farm payroll data, the US Treasury yield curve suggests that investors are pricing in a delay to monetary easing rather than a structural shift toward a high inflation regime.

- Because markets consistently price in prevailing narratives ahead of time, long term investment success depends on objective data and systematic risk management rather than short-term headlines

Geopolitical Progress Eases Energy Supply Pressures

The most significant geopolitical development during May was the progress toward a ceasefire agreement between the United States and Iran. Although the agreement had not been formally ratified by month end, the direction of negotiations became sufficiently clear for markets to begin pricing in a normalization of energy supply conditions.

The original conditional ceasefire, brokered by Pakistan, commenced on 8 April 2026. On 29 May, both parties agreed to extend the arrangement for a further 60 days while gradually easing restrictions on shipping through the Strait of Hormuz.

The announcement triggered a dramatic reversal in energy markets. Brent crude oil fell to US$97.27 per barrel by month end, representing a decline of 29.31% during May. This was the largest monthly decline since the COVID-19 market shock in 2020 and reflected investor expectations that supply disruptions would ease significantly should the ceasefire hold.

Global Equity Markets Driven Higher by Tech Momentum

The sharp decline in oil prices provided an additional tailwind for global equity markets, which were already accelerating on the back of blockbuster corporate earnings and an unprecedented capital expenditure cycle into artificial intelligence technologies.

In the US, investor enthusiasm for the structural buildout fuelled broad market gains. The S&P 500 advanced 5.15% during the month, while the tech heavy Nasdaq Composite outperformed with a stellar gain of 8.36%, lifted by exceptional corporate earnings from major chipmakers and software providers. The Dow Jones Industrial Average also delivered a solid, steady performance, rising 2.78%.

This momentum was even more pronounced across Asia, where key benchmark indices outpaced their US counterparts due to their critical positions in the global technology supply chain. South Korea emerged as the strongest performing major market globally, with the KOSPI surging 28.45%. This extraordinary rally was spearheaded by industry leaders, as Samsung Electronics jumped 43.76% and SK Hynix skyrocketed 81.42% to meet insatiable global demand for advanced high bandwidth memory products.

Similarly, Japan's Nikkei 225 advanced 11.18%, while Taiwan equity markets enjoyed a significant boost from elevated global capital spending on hardware infrastructure.

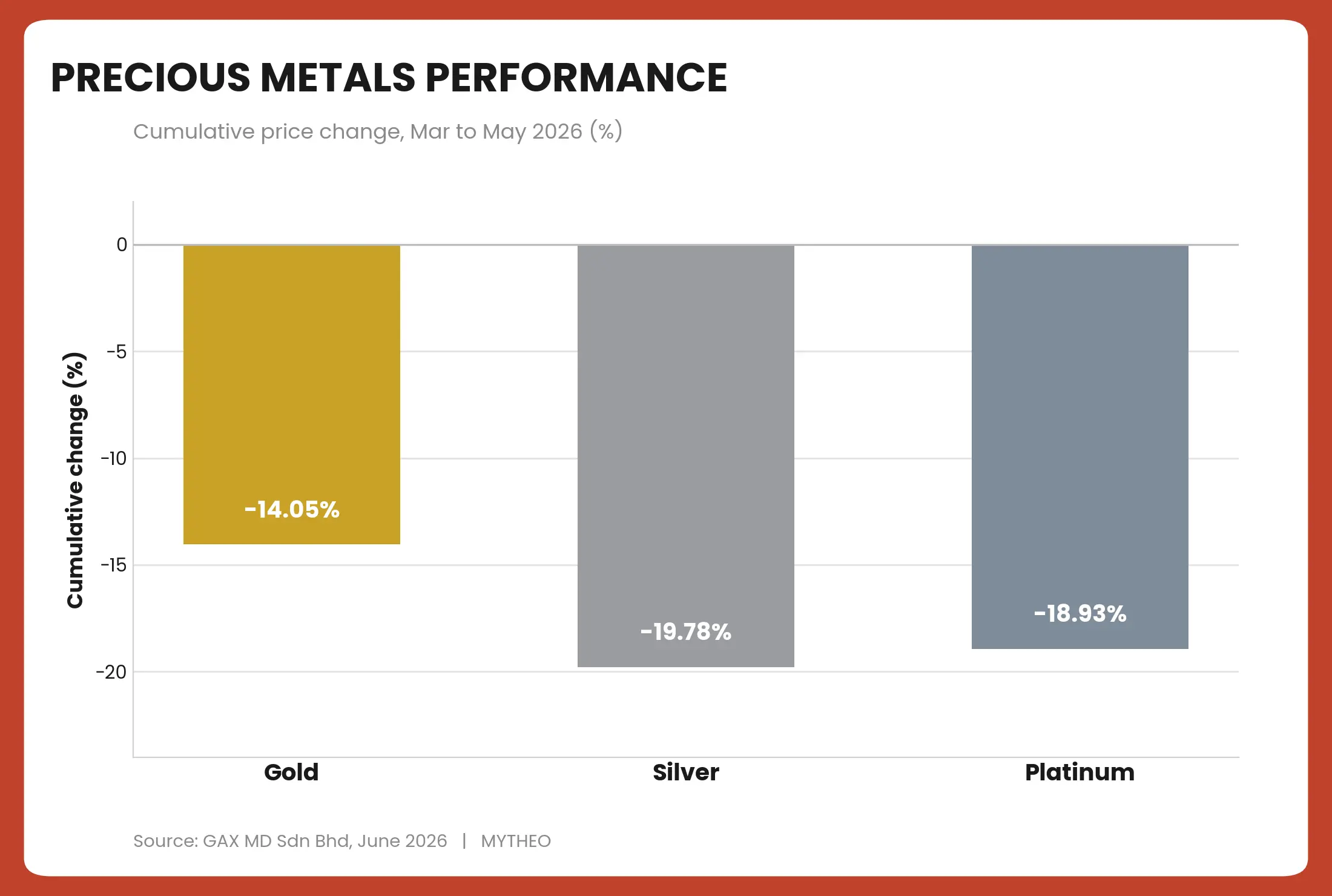

Precious Metals Face Extended Correction

The weakness in precious metals extended into May as investors continued to unwind safe-haven positions following easing geopolitical tensions and improving risk sentiment across global equity markets. Gold declined a further 1.86% during the month, marking its third consecutive monthly decline. Platinum also remained under pressure, falling 3.45%.

Silver, however, provided a notable exception, rebounding into positive territory after suffering losses in the previous two months. Despite the recovery of silver, the broader precious metals complex remained firmly in correction territory. Over the past three months, gold, silver and Platinum have recorded cumulative declines of 14.05%, 19.78% and 18.93%, respectively.

**Past performance is not an indication of future performance.

Inflation Fears Return, but Bond Markets Remain Sceptical

Despite strong equity market performance, inflation returned as a primary concern for investors. US Consumer Price Index (CPI) inflation accelerated from 3.8% in April to 4.2% in May, marking the highest reading since May 2023. The increase reignited concerns that inflation may remain above the Federal Reserve's target for longer than previously expected.

Minutes from the Federal Open Market Committee (FOMC) meeting, released on 20 May, revealed growing concern among policymakers regarding persistent inflationary pressures. Several committee members indicated that additional policy tightening could become necessary should inflation fail to moderate in the coming months.

Reflecting these concerns, bond markets repriced interest-rate expectations, 2-year Treasury yield increased from 3.89% to 4.01%, moving back above the psychologically important 4.0% level. Interestingly, the reaction was far more muted at the long end of the yield curve. The US 10-year Treasury yield increased only modestly from 4.39% to 4.45%, despite rising inflation concerns. The magnitude of this 10-year increase was less than half that of the 2-year Treasury yield shift.

This divergence suggests that while investors have become less confident about the timing of near-term Federal Reserve rate cuts, they remain relatively unconvinced that the recent inflation resurgence will persist over the longer term. In other words, bond markets appear to be pricing in a delay to monetary easing rather than a structural shift toward a significantly higher inflation regime.

Resilient US Labor Markets Trigger Renewed Market Volatility

Market volatility intensified on June 5 following the release of stronger-than-expected US non-farm payroll data. The report showed employment growth of 172,000 jobs, substantially exceeding consensus expectations of approximately 85,000. Rather than viewing the data as evidence of economic strength, investors interpreted the combination of resilient labour markets and elevated inflation as reducing the likelihood of near-term Federal Reserve rate cuts. This led to one of the sharpest daily markets sell-offs of the year as investors reassessed the trajectory of monetary policy.

Mega IPOs Capture Investor Attention

While macroeconomic developments dominated headlines, investors also closely monitored two landmark capital market events. SpaceX completed one of the largest public offerings in market history at an estimated valuation of approximately US$1.75 trillion. Meanwhile, Anthropic filed for a public listing with market estimates approaching US$1 trillion. These offerings have reignited debate over whether large IPOs could temporarily absorb market liquidity or instead reinforce investor confidence in the long-term growth prospects of the AI and space economy.

At this stage, it remains premature to draw definitive conclusions. The eventual market impact will depend on valuation levels, investor demand, and the companies' ability to sustain their growth trajectories after listing.

MYTHEO Investment View

While inflation has re-emerged as a market concern, we believe the recent acceleration is largely linked to energy-related factors rather than a broad-based resurgence in underlying inflation.

**Past performance is not an indication of future performance.

The rise in inflation coincided with a sharp increase in crude oil prices earlier this year, when Brent crude briefly exceeded US$137 per barrel. As energy prices moderate following the Iran ceasefire developments, inflationary pressures may also begin to ease. This suggests that current inflation dynamics are more cyclical and externally driven rather than deeply embedded within the broader economy.

Similarly, we believe the market reaction to the latest non-farm payroll data may have been somewhat exaggerated. Employment growth of 172,000 jobs is well within the historical range of monthly payroll outcomes and does not, in isolation, signal a fundamental shift in labour market conditions. Over the past five years, monthly payroll changes have ranged from negative readings to gains exceeding 900,000 jobs, with an annual average of approximately 254,000.

**Past performance is not an indication of future performance.

Looking ahead, the trajectory of oil prices remains a key variable for both inflation and monetary policy expectations. However, this path remains highly dependent on geopolitical developments in the Middle East, making short-term forecasts inherently uncertain.

Financial markets do not always move in line with prevailing headlines or investor expectations. A common belief over the past several years has been that global central banks are gradually diversifying reserves away from US Treasuries and increasing allocations to gold. Many investors therefore assume that weakening confidence in US government debt should automatically translate into stronger performance for precious metals.

Recent market performance suggests otherwise. Despite continued central bank demand for gold, precious metals have remained under significant pressure. Gold has now recorded three consecutive monthly declines and entered a bear market, while platinum and silver have also experienced substantial corrections over the past three months.

In contrast, US Treasury bonds have demonstrated greater resilience than many investors anticipated. Despite persistent fiscal deficits, uncertainty surrounding Federal Reserve interest rates, and the recent spike in US inflation, longer dated Treasury yields have risen only modestly relative to the scale of negative headlines surrounding the asset class.

The key lesson for investors is that markets often move ahead of prevailing narratives. By the time a particular investment theme becomes widely accepted, much of the expected outcome may already be reflected in asset prices. Rather than relying solely on popular narratives, investors should focus on actual market behaviour and underlying fundamentals. Recent performance highlights that the investment case for gold and Treasury bonds is more nuanced than a simple choice between one asset class and the other.

At MYTHEO, our investment decisions are guided by combining investor risk profiles with the relative risks observed across different asset classes. This helps ensure that investment outcomes remain anchored to long term objectives rather than short term sentiment or headline driven speculation. Whether the debate centres on inflation, interest rates, or high-profile IPOs, our investment process remains grounded in objective market data, consistent diversification, and systematic portfolio construction.

Importantly, our portfolio models have been stress tested across multiple market cycles dating back to 2006. This includes the Global Financial Crisis in 2008, the Covid-19 crisis, the inflation shock following the Russia Ukraine conflict in 2022, and the global trade disruptions associated with international tariff policies in 2025. We believe this long term, evidence-based approach remains the most reliable way to help investors achieve their financial objectives while managing risk through changing market conditions.

Ready to explore how MYTHEO works for your goals? Learn more here.

Or download our app so you can start investing in a moment. Download on iOS here or Android here.

To register for MYTHEO, you can get started here.

This material is subject to MYTHEO’s Notice and Disclaimer.