Monday, 22 March 2021

Written by Amirudin Hamid, Portfolio Manager of GAX MD

The market performance in February 2021 was almost exactly the same as that of in January. The equities started well into the month and rallied higher, only to be halted by a panic sell-off right at the month end due to triggers by the persistent rise in US Treasury yields.

For the most part of the month, the investors’ sentiment was positive and on 16 February 2021, the S&P 500 Index hit 3,950.43 which was a new all-time high. The rally seemed to have been further supported following the testimony by the Federal Reserve’s Chairman, Jerome Powell on 23 February 2021 where he deliberated that the Federal Reserve will not raise the interest rate any time soon until the US economy returns back to full employment. Furthermore, Mr Powell reassured investors that the Quantitative Easing (QE) programme to buy treasury and mortgage-backed securities will continue at the current pace of US$120 billion a month.

However, things turned sour near the month end as the global equity and bond markets were in turbulence after investors went into panic mode when the US 10-year Treasury yield rose sharply and traded above 1.50% for the first time since February 2020. A surge in yield usually reflects that the economy is expected to grow at a much faster rate than initially thought and will be exposed to more inflation risk. And when this happens, central banks around the world may be forced to shift towards tighter policies and eventually raise interest rates. A higher interest rate makes bonds more favourable compared to equities, especially the high-growth technology stocks that have been trading at steep valuations after strong rallies in the past twelve months. That is why the high-flying technology stocks skidded erratically near the end of the month as investors used inflation fear as an excused to lock-in profits.

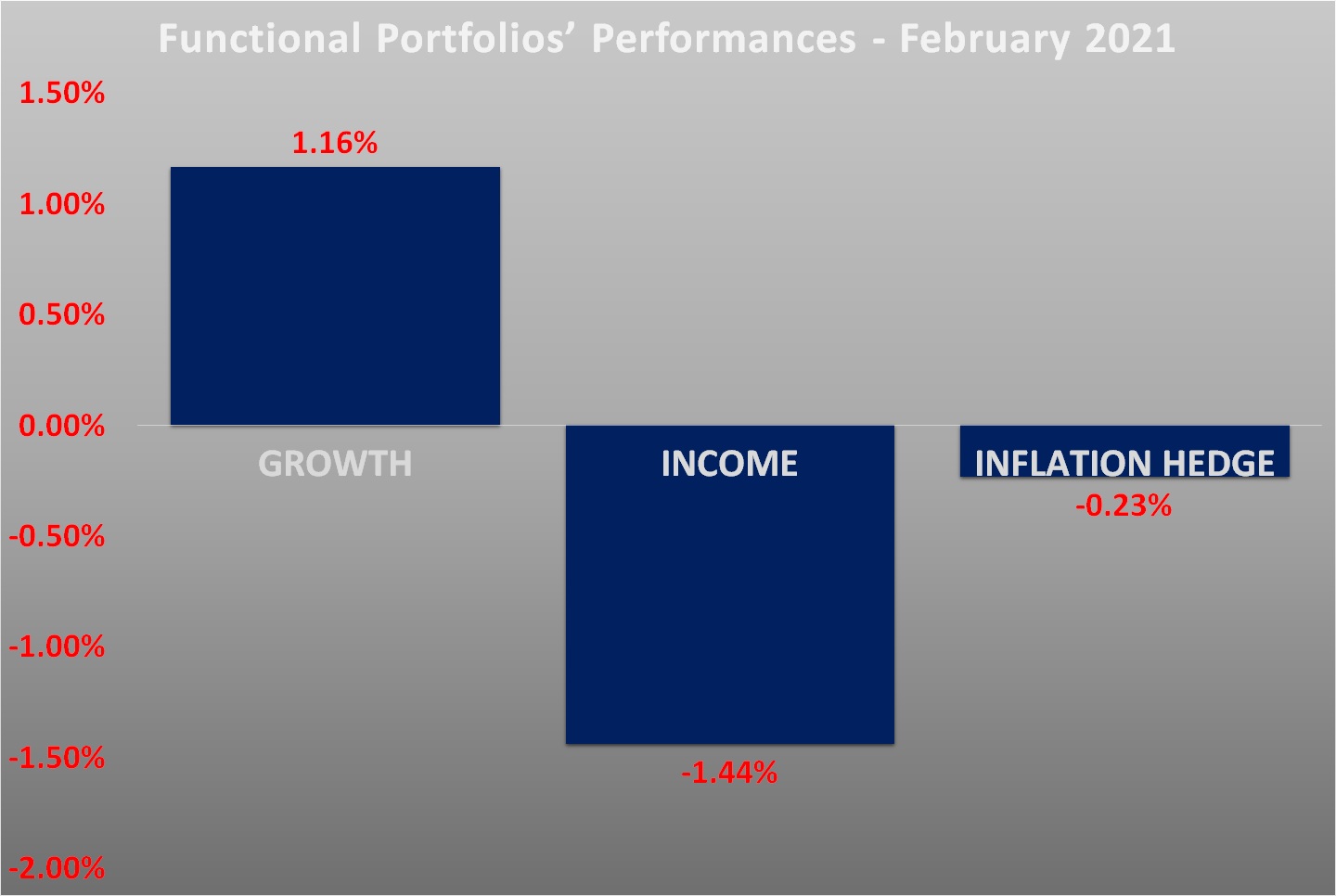

The Growth portfolio rose by 1.16% while Income and Inflation Hedge portfolios declined by 1.44% and 0.23% respectively.

Chart 1: Functional Portfolios’ Performances for the month of February 2021

Source: GAX MD Sdn Bhd, March 2021

Note: Past performance is not an indication of future performance

The GROWTH portfolio rose by 1.16% in MYR

The Growth portfolio chalked up a modest gain in February 2021, which was due to the strong run-in earlier part of the month. Taiwan stocks (EWT) continued a strong performance by adding another 5.88% driven by the performance of technology stocks. It was followed by value stocks in the US (VTV) and Hong Kong stocks (EWH), which rallied by 5.25% and 5.24% respectively. Both VTV and EWH benefitted from the rotational play by investors who switched from high-flying technology stocks to financial and banking stocks that were trading at much cheaper valuations.

Inside the Growth portfolio, only China stocks (FXI) and Frontier Market stocks (FM) dropped into negative territory in February but losses on both were marginal at -0.35% and -0.17%, respectively. FXI was affected by the slower expansion of factory activity in China. The data from the National Bureau of Statistics of China (NBS) showed that the Purchasing Manager’s Index (PMI) in February fell to 50.6 from 51.3 in the previous month.

Small losses on FM came purely from profit-taking activities. The ETF has performed so well in the past few months and was one of top three best performers inside the Growth portfolio in January.

The INCOME portfolio dropped by 1.44% in MYR

The US Treasury was a major talking point in February. Finally, investors felt the heat of a rising yield when the 10-year Treasury yield surged above 1.5%, reflecting expectations of a higher inflation and higher borrowing costs for companies and individuals.

As a consequence, all assets inside the Income portfolio were valued lower in February compared to a month earlier. Assets with a longer time to maturity are more sensitive to the movement of the interest rate, hence, they were impacted more than assets that have a shorter time to maturity. The US Treasury with more than 20 years to maturity (TLT) and International Treasury bond (IGOV) had the steepest fall of all after the price were down by 5.50% and 2.49% respectively. TLT has an effective duration of 17.3 years and IGOV has an effective duration of 9 years.

On the other hand, assets with a shorter time to maturity had smaller losses. In MYTHEO’s portfolio holdings, Treasury Bond with 3 to 7 years to maturity (IEI) and Intermediate-Term Treasury (VGIT) fell only by 0.86% and 1.14% respectively. IEI has an effective duration of 4.6 years and VGIT has effective duration of 5.3 years.

The INFLATION HEDGE portfolio dipped by 0.23% in MYR

The Inflation Hedge portfolio dropped marginally in February 2021. Drilling down further, the performances of the underlying assets inside the portfolio were mixed in an extreme way. On one side, Crude Oil (DBO), Metal (DBB) and Real Estate Mortgage (REM) flew high with outsized returns of 16.80%, 11.38% and 8.95% respectively. All these assets were viewed by investors as best assets to own in the high inflation environment.

On the other side, Clean Energy (ICLN) and Gold (IAU) were hit quite badly after their share prices dropped by 13.04% and 6.10% respectively. Despite a big loss, the correction in ICLN’s share price was merely due to profit taking as the ETF has performed extremely well and even after the correction, it has gained more than 150% over the past 12 months. Meanwhile, IAU retreated mainly because the higher bond yield made gold less appealing to investors.

It must be noted that, the actual portfolio returns to the investors is the combined weighted return from the allocation to each functional portfolio. For example, if an investor allocates the investment 40% in Growth, 40% in Income and 20% in Inflation Hedge, the actual portfolio return is (40% x 1.16%) + (40% x -1.44%) + (20% x -0.23%) = -0.16%

Note: Past performance is not an indication of future performance

Our thoughts

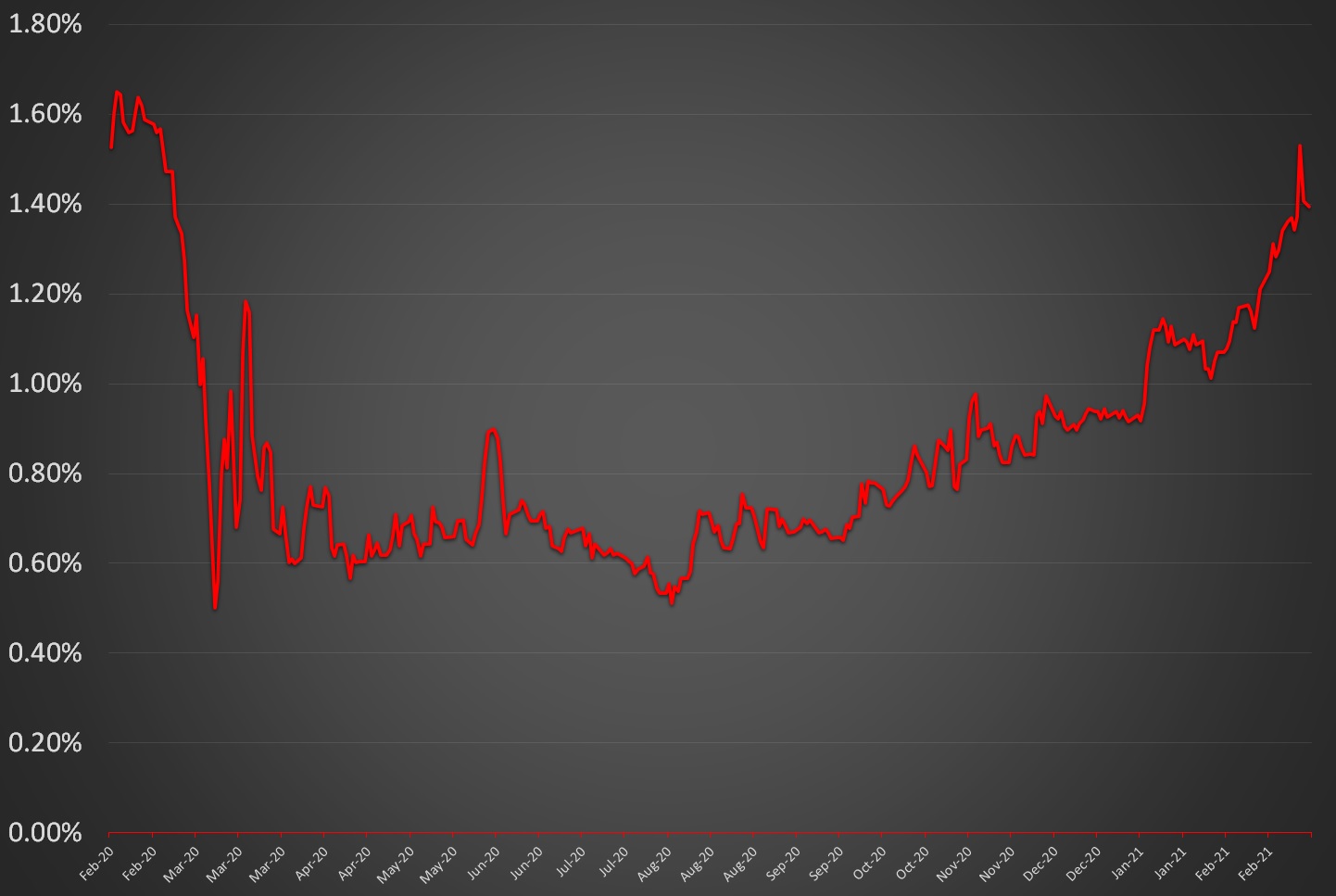

The market scenario is much different than what many investors had expected exactly a year ago. In February 2020, the economic and financial markets were faced with the rising threat of the COVID-19 infection. Some you may recall that many investors were so sceptical of the market rebounding and the economy recovering. Rather, many had feared that economic activities would slow further and prolonged asset deflation was inevitable. At that time, any advice that passed through our ears mostly told us to stay defensive and to allocate more into safe-haven assets to avoid further losses. In the extreme, economists were debating that the Federal Reserve may adjust the interest rate to negative.

Chart 2: US 10-Year Bond Yield from February 2020 to February 2021

Source: Investing.com, March 2021

Note: Past performance is not an indication of future performance

Today, it seems that such fear has been forgotten and thrown out of the mind of many investors. Ironically, investors are concerned about inflation risks today as compared to deflation risks previously. This indicates how fast the market view has changed. Out of a sudden, inflation has become a hot topic in the market, which was triggered by the rise of the US 10-year treasury yield.

The past twelve months have been eventful and there are plenty of valuable lessons for all investors. One of which that we have kept repeating constantly, is that the financial market is so unpredictable. The scenario that you are in today is not necessarily the same for tomorrow. Likewise, in investing, assets that perform badly today will not necessarily perform badly in the future.

Therefore, to achieve better success in investing, do not shift asset allocations based on the momentum of the market today. Focus on your long-term objective and try to see past the noise and volatility in the market. By doing so, you can have a better success of achieving your long-term financial objective. Thus, worry not as MYTHEO has been developed and formulated to support this investment strategy.

Disclaimer: This material has not been reviewed by the Securities Commission Malaysia. MYTHEO investors may still be exposed to investment risks. Future investment returns cannot be guaranteed.