MYTHEO is a digital investment management service that provides users with tailored, professional level investment services through the use of leveraging technology.

The investment technology used by MYTHEO was originally developed in Japan by Money Design Co., Limited. The strategy has been live in Japan since February 2016 and is currently used to provide high-quality investment services to over 100,000 Japanese investors.

MYTHEO uses the same underlying technology as the Japan strategy but has been tailored to meet the needs of Malaysian investors.

The key characteristics of MYTHEO’s investment strategy are as follows:

I. Introduction to Investing

This section discusses some of the investment concepts used by MYTHEO.

Diversification

In investing, diversification is a process whereby investments are spread across regions, assets and time. This diversifies the risks of individual investments and reduces the overall risk of the portfolio.

There are 3 types of diversification:

References

Malkiel, B.G. 1996. "A Random Walk down Wall Street: The Best Investment Advice for the New Century", W.W.Norton&Co., New York.Vanguard. 2012. "Dollar - cost averaging just means taking risk later", Vanguard Research

ETFs

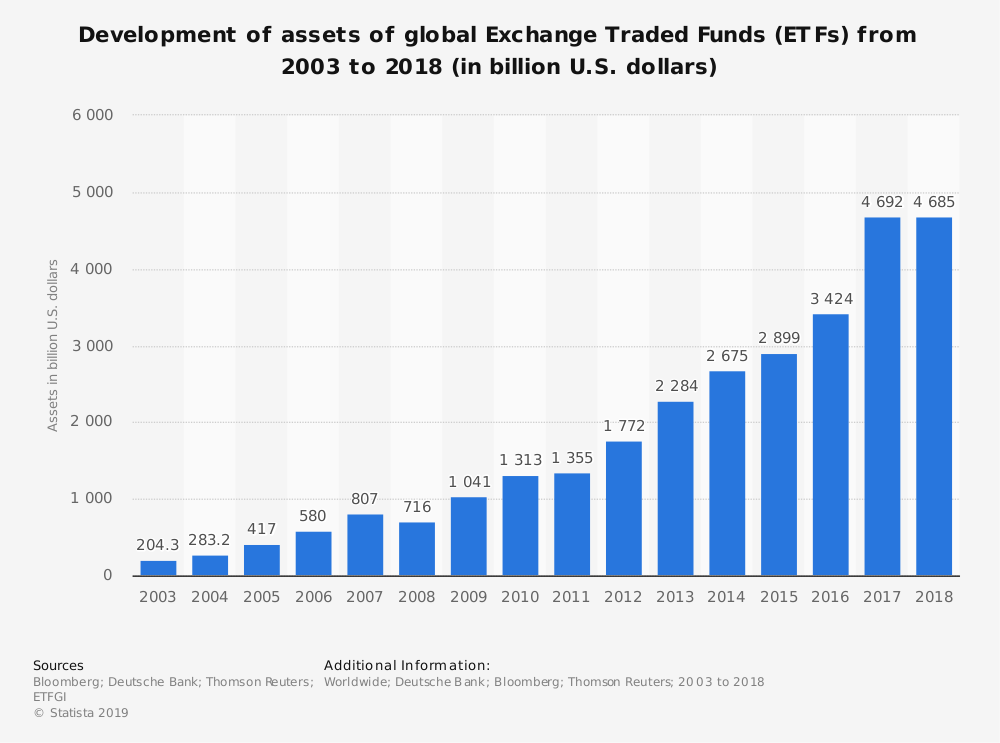

ETFs (Exchange-Traded Funds) have been called "one of the biggest financial inventions of the 20th century” and they are considered to be the most suitable tool for constructing an efficient portfolio. About 6,000 ETFs are listed on stock exchanges all over the world and they are widely used by institutional and individual investors.

Most ETFs are linked with indexes such as stock price indices and many ETFs correspond to specific asset classes. Therefore, if you use ETFs, it is possible to invest in a diversified range of assets such as stocks, bonds, REITs (real estate investment trusts) and commodities (goods) at low cost.

ETFs are said to have low trading and holding costs compared with unit trusts and because they enable diversification across a wide range of asset classes, they are seen as an attractive vehicle for long-term investing. In addition, since they are listed on exchanges, they are highly liquid. The ETF market is expanding year by year and the expansion is expected to continue in the future as well.

MYTHEO mostly invests in ETFs listed in the USA as markets there have many different types of ETF. MYTHEO selects the ETFs that are most suitable for customers to be included in the investment universe (Refer to Section III: Investment Approach: Selection of ETFs for further details).

Smart Beta

Smart beta refers to the return obtained, in addition to general movement of the market, from investing in factors such as size (e.g. small stocks) and value (e.g. cheap stocks) that have a risk premium.

This approach is widely used by institutional investors. For example, the Teachers Insurance and Annuity Association of America (TIAA), the California State Teachers' Retirement System (CalSTRS) and the Japan Government Pension Investment Fund (GPIF) all use this approach.

Although there is no universally accepted definition of smart beta, it is often taken as an index that does not rely on market capitalization weightage. For example, using objectively measured fundamental indicators such as corporate profits, sales volume or stock indicators such as Price to Book or Price Earnings Ratio.

More generally, smart beta usually refers to measures that:

For details on how MYTHEO uses smart beta, please refer to Section II: Investment Model.

References

Fama, E.F., French, K.R. 1993. "Common risk factors in the returns on stocks and bonds", Journal of Financial Economics 33.

Compound Return Effect from Reinvestment

Reinvestment means re-investing profits (such as dividends received) back into the portfolio. It is an investment method that aims at capturing the compound interest effect.

There is a famous story about the power of compound interest relating to Manhattan Island. The island was originally held by native Americans who sold it to the Dutch settlers in 1626 for only $24. If the native Americans had invested the $24 in assets yielding 6% per year and reinvested the profits, the assets would now be worth around $200 billion today! Of course, it is not certain that there are assets that will yield 6% for nearly 400 years. However, if turn to the 6% yield each year, after the first year the value of the portfolio will be 24 + 1.44 = 25.44, the next year investment principal increases so the 6% yield also increases and the value of the portfolio after the second year becomes 25.44 + 1.5264 = 26.97. This is the effect of compound interest from reinvestment.

Reinvestment can be very effective if you are planning to invest for medium to long-term. For example, RM1 million invested with a yield of 6% and reinvesting the yield yields RM1.39 million in 5 years and RM1.79 million in 10 years. However, in order to maintain diversification while reinvesting, the reinvestment allocation must be appropriate. The MYTHEO algorithm reviews the asset allocation of each user and when a dividend has been received, it reinvests in the appropriate allocation for the customer.

Functional Approach in Portfolio Management

Traditional asset management relies on categorizing investments based on the type of asset or the expected return and risk. The types of asset classes include stocks or bonds or regions such as developed markets and emerging markets. The investment approach includes passive, active, absolute return or balanced investment strategies.

However, recent discussion on the classification of financial services has focused on the objectives or function of the services and investment services based on the needs of customers have started to develop. Discussion of the asset classes or risk levels are important for the customer to understand the performance characteristics of the investment service, but they do not actually reflect the needs of the customers. Each customer may have different investment objectives and it is necessary to design the investment service to reach those objectives. Therefore, an investment approach based on the needs of the customer is required with portfolios constructed based on these needs rather than asset types.

For example, in CalPERS, the largest pension fund in the US, the investment objectives are grouped based on "Growth", "Income", “Real Assets", “Liquidity" and "Inflation". Growth is composed of listed and unlisted equity with the objective of earning a high return. Income is composed of domestic and international bonds with the objective of lowering risk while also improving the rate of return. The Real Assets category includes real estate, forest land and infrastructure with the aim of earning returns that are more resilient to inflation than bond returns. The Liquidity category includes cash or cash substitutes that are used to meet the payment needs of the pension fund. The Inflation category includes inflation-linked bonds and commodities to protect against inflation and diversify the sources of income.

MYTHEO uses 3 functional portfolios to meet customer needs for Growth, Income and Inflation Hedge. Each customer portfolio is made up of a combination of these 3 functional portfolios. The Growth portfolio invests mostly in a global range of equity ETFs in order to achieve high returns over a long-term period. The Income portfolio invests mostly in a global range of bond ETFs in order to achieve stable returns with low risk. The Inflation Hedge portfolio invests in real asset or inflation related ETFs such as commodities, real estate of inflation-linked bond ETFs to try and earn a higher return than Malaysian inflation while also keeping a low correlation with the global equity market. By using these 3 functional portfolios, MYTHEO makes it easier for customers to achieve their investment goals.

Reference

CalPERS, 2010.11, ALM Workshop

US Dollar – Denominated Investments

MYTHEO receives contributions from customers in RM then exchanges it into US Dollars in order to purchase the ETFs. As a result, customers are impacted by movements in the RM/USD exchange rate.

MYTHEO purchases ETFs that invest in a wide range of countries and regions around the world. These ETFs are exposed to the currency of the country/region in which they invest in and hence MYTHEO’s actual currency exposures are diversified.

II. Investment Model

This section explains the objectives and models behind MTHEO’s three function portfolios and AI Assist.

Growth Portfolio

The goal of the Growth portfolio is to obtain high returns on a long-term basis in line with the global equity market. In order to achieve this, the portfolio invests in assets with a high long-term rate of return, i.e. stocks. In addition, the portfolio is diversified across a range of countries.

According to Ibbotson, the long-run return (geometric mean) of US large-cap stocks from 926 – 2013 was 10.1%. This is much larger than the return for corporate bonds (6.0%) and long-term government bonds (5.5%). On the other hand, stocks have higher volatility (i.e. the price moves are larger) than bonds, so in that sense stocks have higher risk than bonds.

The ideas underlying current investment theory such as Markowitz's portfolio theory and Sharpe's CAPM (Capital Asset Pricing Model) etc. do not necessarily reflect the actual movements of modern financial markets and through such experiences as the Lehman shock, it has been shown that relying solely on existing approaches can lead to large losses. The Growth portfolio utilizes “minimum-volatility” techniques that have received much more attention since the Lehman shock.

The goal of the Growth portfolio is to obtain high returns but the portfolio construction process does not rely on trying to forecast the returns of individual companies etc. which is very difficult to do accurately. On the other hand, optimization methods that aim to minimize risk have been shown to be effective, so the Growth portfolio uses optimization techniques to minimize risk (i.e. return volatility).

The Growth portfolio aims to achieve higher long-term returns than the other functional portfolios by investing in relatively high risk/high return equity ETFs, so it may seem contradictory that it also aims to minimize risk. However, the actual risk of the Growth portfolio is higher than that of the Income portfolio. Compared to other portfolios investing in equity ETFs, the Growth portfolio aims to achieve the lowest possible risk. In addition, when deciding the final weightage of ETFs in the Growth portfolio, MYTHEO uses measures such as Valuation (i.e. is the ETF relatively cheap or expensive?) and Momentum (i.e. is the price of the ETF trending up or down?) in order to make tactical allocation decisions.

References

Haugen, R.A., Baker, N.L. 1991. "The efficient market inefficiency of capitalization - weighted stock portfolios", Journal of Portfolio Management, 1991 Spring

Haugen, R.A., Baker, N.L. 1996. "Commonality in the determinants of expected stock returns", Journal of Financial Economics, 41.Roger G. Ibbotson and Rex A. Sinquefield, "the Ibbotson SBBI Yearbook 2016"

Income Portfolio

The Income portfolio is mainly composed of fixed income ETFs and is designed to achieve relatively stable and steadily returns without suffering significant losses. In addition, diversification benefits can be obtained by combining the Income portfolio with the Growth portfolio.

In terms of the contents of the bond ETFs, they are mainly sovereign (i.e. government) bonds, investment grade corporate bonds and mortgage-backed bonds. High yield corporate bonds and emerging market government bond ETFs are also included in the portfolio although the weightages are smaller. The bonds in the ETFs cover a wide range of countries.

In contrast to stocks, investment returns of bonds are closely related to their most recent yields and hence can largely be predicted. On the other hand, incorporating only high yield bonds tend to lead to a high-risk portfolio. Therefore, optimization of the Income portfolio is achieved by maximizing the average bond yield relative to the conditional value at risk (CVaR), subject to a certain duration constraint. The average bond yield is calculated by taking the weighted average yield of the bonds included in the ETF.

Inflation Hedge Portfolio

The Inflation Hedge portfolio is designed to match and exceed the Malaysian inflation rate. Also, it works to reduce the correlation with global stocks and to reduce the risk from major market events. We also invest in ETFs such as crude oil, industrial metals, precious metals, real estate, Treasury short-term government bonds and inflation-linked bonds, in addition to asset classes that are thought to be directly impacted by the inflation rate.

First, we conduct multiple regression analysis of commodity and real estate prices against the inflation rate to determine allocation rates for these ETFs. Annual returns are used in order to match the annual inflation rate and we use overlapping data periods to obtain as many data points as possible. We update this multiple regression analysis quarterly after reviewing cost and hedging effectiveness.

Moreover, we minimize the correlation with global stocks by using ETFs such as precious metals and inflation-linked bonds. In this case, we avoid holding too many illiquid ETFs by setting upper limits on the weight of low-liquidity ETFs.

Artificial Intelligence (AI) Assist

MYTHEO’s AI Assist refers to the use of AI to try and predict whether an ETF or asset class is at risk of a large drawdown in the near future based on data from Thomson Reuters MarketPsych Indices (TRMI) and market data. If AI Assist decides that the risk is high, we will set the portfolio's optimization parameters to a more conservative one and hence aim to reduce the downside risk of the portfolio. The aim of introducing MYTHEO’s AI Assist is to improve the mid-to-long term performance of the portfolio by reducing downside risk.

MYTHEO is managed using a model built on a quantitative analysis. Quantitative investment management does not depend on the predictions or decisions of fund managers and thus, the models can easily be back-tested. In that sense, one of the advantages of quantitative investment management is that it does not depend on the fund manager.

Most traditional investment models only use market data for each asset and index. This data does have some ability to predict future market movements but market sentiment, as formed by news and social media, also influences market movements. For example, despite many article claiming that “stock prices are too high”, stock markets continued to rise from autumn 2017 until the market actually fell sharply in February 2018.

Without the use of tools such as MYTHEO’s AI Assist, it is difficult to incorporate market sentiments into the model for the following reasons:

In order to incorporate market sentiment into the model without relying on the interpretation of fund managers, we use Thomson Reuters MarketPsych Indices (TRMI) data. Based on the proprietary research of MarketPsych, this gives measures of market sentiment for many assets based on text mining and scoring techniques that use large-scale natural language processing. Over 40,000 major global news sources and 7,000 blogs and social media sites are covered. Using this data helps to overcome problems (a) and (b) above.

With MYTHEO’s AI assist implemented in the portfolio, we expect that the downside risk of the portfolio is reduced and which in turn improves the long-term performance.

III. Investment Approach

In this section, we will discuss how the customer's assets are actually invested by MYTHEO based on the investment model described in the previous section.

Portfolio Diagnosis

In MYTHEO, we first ask customers five (5) questions via the MYTHEO app or website to assess the investment needs of the customer. Based on the answer to the questions, we will propose an optimal portfolio for the customer.

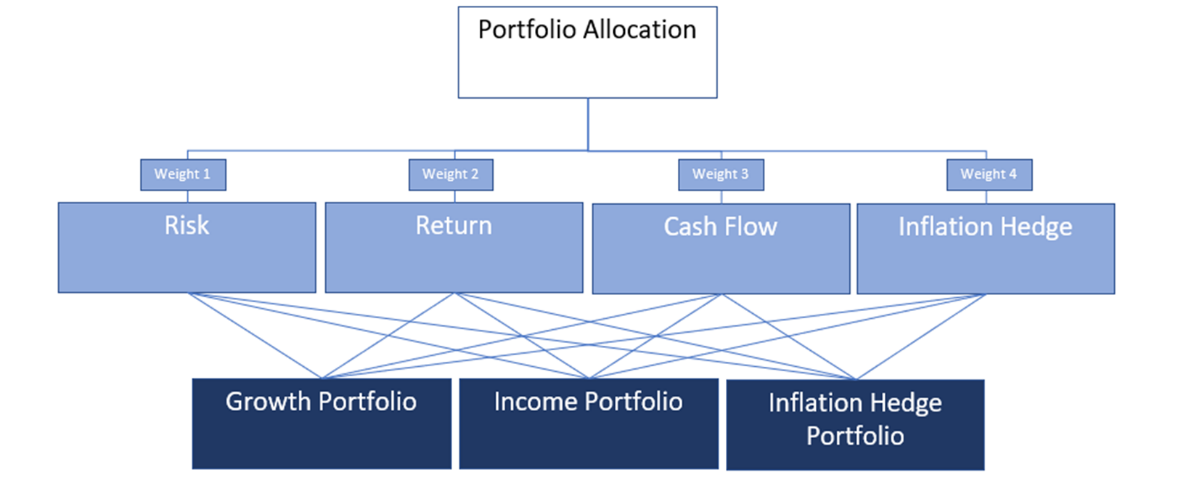

The diagnosis is carried out by MYTHEO's proprietary process. In traditional asset management, the portfolio (i.e. the weightage of each asset) is calculated based on the risk and the expected return. In MYTHEO, we utilize the three functional portfolios as described in the section above. We aim to create an optimal portfolio by combining these functional portfolios to meet the investment objectives of the customer. Therefore, the results are different from traditional asset managements which use quantitative methods focused solely on risk and return. In order make investment decisions where there are multiple investment objectives, we use a technique called Analytic Hierarchy Process (“AHP”).

Customers are asked the following five (5) questions:

Based on these questions, we use AHP to estimate how important each investment objective is for the customer and calculate the optimal weightage of the three function portfolios to match these objectives. AHP uses for investment elements: expected return, risk, cash flow and inflation hedge. We use the profiling questions to measure the relative importance of each element for the customer. Then we use the relevance of each functional portfolio for these elements to calculate the optimal functional portfolio weightage for the customer. Besides that, customers can choose to customise the weightage of their functional portfolios. The total number of different portfolio combinations available for customers are 373.

For more details on AHP, please refer to the paragraphs below.

Supplement: Analytic Hierarchy Process

AHP is a decision-making method developed by Saaty (1980) to evaluate alternative choices using a hierarchical structure. It is commonly used for decision making where the choices depend on the preferences of individuals. In MYTHEO, we divide the decision-making process into multiple hierarchies and quantitatively measure the importance of each evaluation factor for each level in the hierarchy and apply the user preferences obtained from the profiling questions.

In AHP, the overall structure of multiple hierarchies is decided first. At the top of the hierarchy is the decision goal i.e. the optimal allocation across functional portfolios. The second level includes the four (4) investment elements (risk, return, cash flow, inflation hedge) and the third level includes the three (3) functional portfolios.

Next, the relationship between the investment elements and the functional portfolios is determined. Each relationship pair is assigned a numerical value based on the relative importance of the two (2) alternatives as regards each investment element (e.g. alternative A is much more important than alternative B for this investment element, more important, slightly more important, the same etc.). Subsequently, we measure the general relationship between alternatives for each element. Through this, we can compare all the pairs based on the characteristics of each of the three (3) alternatives with respect to the four (4) elements.

After that, for each hierarchy, weightages are calculated based on the weights of the alternatives in the lower level hierarchies. Through this, the optimal portfolio weightage for the customer can be calculated.

References

Saaty, T.L. 1980. "The Analytic Hierarchy Process", McGraw - Hill

Selection of ETFs to be Included in the Investment Universe

MYTHEO selects ETFs, mainly from the US, that meet the investment requirements set by MYTHEO and these are incorporated into the investment universe.

The expenses of the ETF such as management fee, accounting costs, taxes, legal and audit costs are set by the ETF's investment management company (generally indicated as an annual rate, referred to as the ETF expense ratio) and they are deducted from the Net Asset Value (NAV) of the ETF. For clarity, NAV is the total amount of underlying assets of ETF (minus debt, if applicable) divided by number of ETF units in issue. The NAV is updated every 15 seconds during trading hours. As ETFs are financial instruments traded on the stock market, purchasing or selling of ETF units occur at the market price, not the NAV, but the market price reflects the NAV and so the customer can be said to indirectly bear the ETF expenses as a result.

If a certain sub-category is included in our investment strategy, but there is no suitable ETF, an ETF that is as close as possible to the sub-category may be used instead. However, an upper limit is placed on the weightage that can be allocated to such an ETF. Regularly (at least annually) we review all listed ETFs that are not included in the investment universe so far. We investigate whether there are ETFs with similar features but lower expenses than the ETFs currently in the investment universe. Furthermore, we continually monitor the investment universe to check that all the ETFs in the investment universe continue to meet the investment requirements.

New ETFs are listed every year and the ETF market continues to grow. We add new ETFs into the investment universe when appropriate and also remove ETFs, for example if the liquidity has declined.

Supplement: ETF Trading Costs

The difference between the selling price (Bid) and the purchasing price (Ask) is often referred to as a hidden cost of trading.

MYTHEO buys and sells ETFs through the listed market and aims to sell at as high a price as possible and buy at as low a price as possible so this difference is referred to as the Bid/Ask spread. In the case where the traded volume of an ETF is small (i.e. liquidity is low), the spread becomes wider i.e. you must purchase at a relatively high price and sell at a relatively low price so the trading cost is high. As the purchase is made using the customer’s money, the customer bears this cost. For example, if send ETF trade orders as “market orders” i.e. buying and selling at any price, there is a large risk of buying at a high price and selling at a low price.

In MYTHEO, we use an algorithm to trade when these Bid and Ask prices are as close as possible.

For further details, refer to Section III: Trading: Trade Execution below.

Trading

Portfolio Composition

When there is a contribution from a customer, we purchase ETFs in line with the customer’s allocation of functional portfolios. The ETF purchase procedure is outlined below:

In the case of MYTHEO, if the day on which the contribution was made is a business day in Malaysia and the US, steps (1) to (3) occur on that day (for initial contributions it is on the following business day). MYTHEO could have contributions from many customers each day so MYTHEO executes these orders in bulk at IB in order to trade as efficiently as possible.

Algorithm to Calculate the ETF Order Quantity

In MYTHEO, we calculate the order quantity for each ETF using a proprietary algorithm. Different customers' target weightage for each ETF are calculated from the customer's target portfolio recommended based on AHP and the weightage within each functional portfolio determined by the investment algorithm and the market price of the ETF at the time of the transaction.

Trade Execution

Trade execution is performed by a proprietary algorithm. Once the US stock market opens (22:30 in Malaysia, 21:30 during US summer time), we decide the ETF trade amount for each customer by using the latest market price. This is more efficient than deciding the trade amount before the US stock market opens. The ETF trade amount for each customer is calculated instantaneously using the algorithm described in the previous section and is sent to the broker for execution.

In executing, we monitor the difference between the market quote for buys and sells (Bid/ Ask Spread) and in the case where this spread is larger than usual, the order price is adjusted (it is not always possible to trade at a price better than the current market price).

Although, there is a possibility that it may not be possible to trade immediately due to intense price fluctuations, small trading volume, large spreads or large orders etc. However, by using probability filtering and Brownian motion based on past transactions and market data, it is possible to make optimal trade execution decisions.

Portfolio Adjustments

As described above, the target weightage of each ETF per customer is determined from the target weightage of the functional portfolio determined from the customer's profiling and the relative weightage of the ETF within each functional portfolio. In MYTHEO, we regularly rebalance the weightage of the ETFs in each portfolio to keep the customer's portfolio in an optimal condition.

Additional Contributions/ Partial Withdrawals

When there is a request for additional contribution or partial withdrawal from the customer, we will compare the target weightage of each ETF at that time with the current holding weightage of the customer and purchase the ETF that is below the target weightage (in the case of additional contributions) and we will sell the ETF that is above the target weightage (in case of partial withdrawals). This gives customers the same effect as rebalancing i.e. it makes the portfolio more optimal.

Execution Procedures*

In case of contribution

If the customer contributes by 12:00 noon on a business day in Malaysia, the cash is invested in the US on the same day (next business day if the US is on holiday). If it is after 12:00 noon or if a customer contributes on a Malaysian holiday, the cash is invested on the next business day. The number of ETFs purchased will depend on the FX trade from RM to USD.

When there is a partial withdrawal

When a customer requests for a partial withdrawal by 12:00 noon on a business day in Malaysia, the ETFs are sold on the same day (next business day if the US is on holiday). If it is after 12:00 noon or if a customer requests on a Malaysian holiday, the ETFs are sold on the next business day. Proceeds of the ETF sales will be in USD, so the RM amount of the withdrawal will depend on the FX trade from USD to RM. The shortest time by which the withdrawal amount is paid to the customer is three (3) business days.

Cancellation request

If the customer has requested for a cancellation by 12:00 noon on a business day in Malaysia, the ETFs are sold on the same day (next business day if the US is a holiday). After converting the sale proceeds from RM to USD, the proceeds are paid to the customer within seven (7) business days. Depending on the ETFs which are held by the customer, there may be unpaid dividends at the time of the cancellation. In this instance, we will return the funds obtained through the sale of the ETF as normal, and once the dividend is paid, we will also return that to the customer.

User changes to the target weightage of the functional portfolios

MYTHEO will sell and purchase ETFs on the same day the customer makes the changes. By minimizing the time lag between sales and purchases, we minimize risk to customers due to market changes.

*The timings shown here are the expected timings under normal market conditions. Timings may vary due to factors such as liquidity, volatility and market closures etc.

References

De Bondt, Wernar, F.M., and Thaler, R. 1984. "Does the Stock Market Overreact?", The Journal of Finance, vol.40.Poterba, J.M., Sammers, L.H. 1988. "Mean Reversion in Stock Prices: Evidence and Implications", Journal of Financial Economics, vol.22.

Limitations of Algorithms

Functions

As described in this White Paper, algorithms are used by MYTHEO for various functions:

Assumptions and Limitations

These algorithms can be very effective in providing high-quality, consistent, tailored customer portfolios at a reasonable cost while avoiding human biases and behavioral errors. The algorithms are back-tested rigorously against historical data that includes major events such as the Lehman Crisis, the Eurozone Crisis and the Brexit referendum etc. If similar events occur in the future, we expect the algorithm to perform in a similar way to the back-test.

As a result, the main assumption of the algorithms is that events in the future (e.g. inflation, life expectancy, volatility, range of market returns etc.) will not be materially different from what was experienced during the back-tested period. If an event completely different from past experiences occur or there is a major structural change in the market, it is possible that the investment algorithm may perform differently from the back-tested results.

Risks

In addition to the limitations noted above, there are additional risks inherent in the use of technology for investment purposes. Examples of such risks include:

MYTHEO has procedures in place to mitigate these risks:

IV. Investment Policy Committee

In MYTHEO, we have established an Investment Policy Committee which reviews and decides the overall investment policy and asset allocation as well as reviewing investment performance. The committee usually meets monthly and covers the following areas:

Additionally, the committee monitors the portfolios, investment performances and trade executions.

dan mulakan perjalanan pelaburan digital anda bersama MYTHEO!